The average American opens their first credit card at 20 years old. It’s a valuable resource in emergencies and a great way to build a credit history, but is also a source of financial stress for thousands of Americans.

Reducing debt is a priority for 70% of Americans looking to improve their well-being in 2021. This effort shows, as the average credit card debt in the U.S. has decreased $969 since 2019 — a 14.9% improvement.

Understanding how debt accumulates and learning credit card debt statistics can help borrowers review their situation and create a plan to dig out of debt.

Key Findings

- The average American had $5,525 in credit card debt in 2021.

- Credit card debt is the second largest debt source behind mortgage debt.

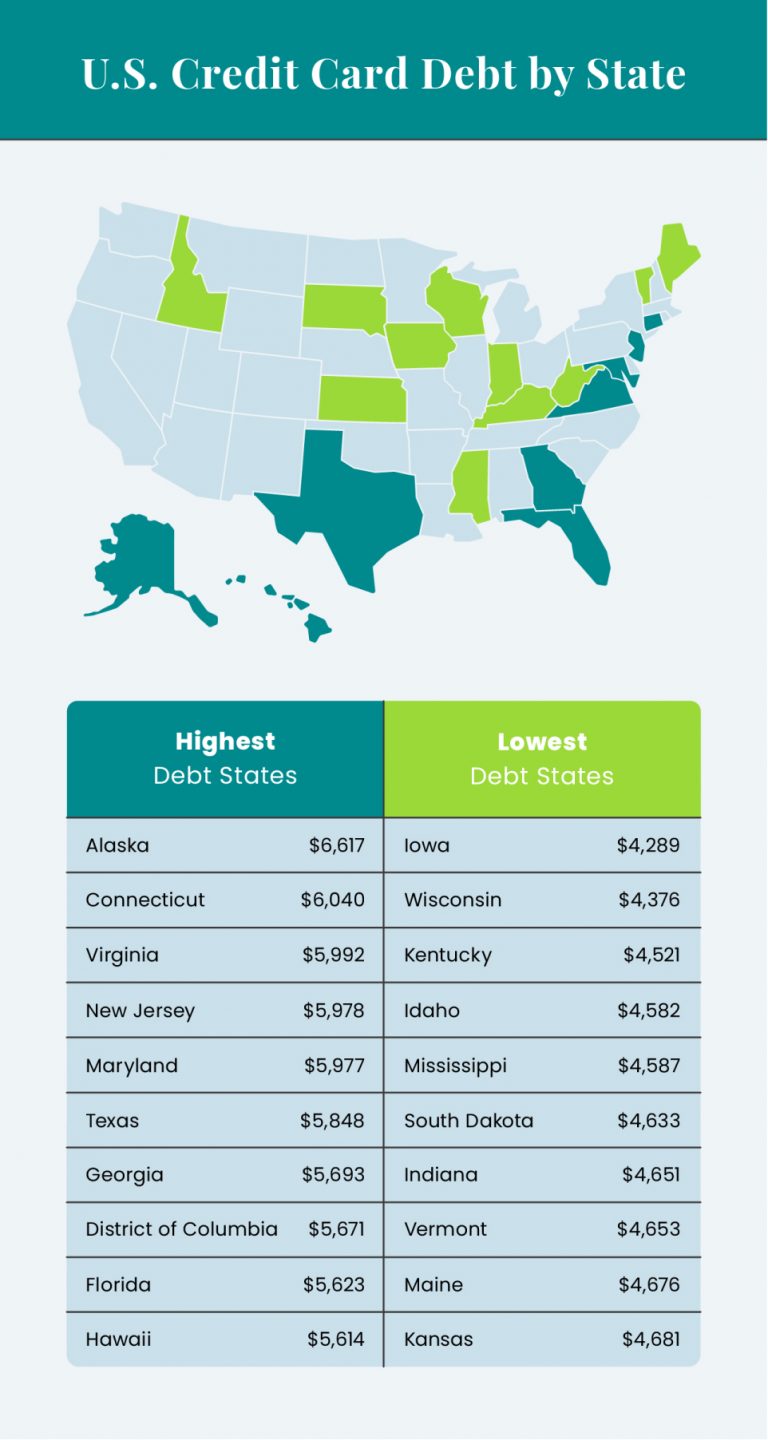

- Alaska has the most credit card debt of any state with $6,617 in 2020 and $7,089 in 2021.

- Iowa has the least debt, with a balance of $4,289 in 2020 and $4,587 in 2021.

- Generation X has the largest amount of credit card debt at $7,236.

- Hispanic Americans have the largest proportion of credit card debt compared to their income at 9.96%.

Average American Credit Card Debt by State

In 2021, the national average credit card balance was $5,525.

Alaska had the highest average balance in the U.S. in 2020, with $6,617, which was 12% higher than the national average of $5,897 for that year.

Generally, states with high costs of living have higher average balances, including Alaska, Connecticut, District of Columbia (D.C.) and Hawaii in the top 10 highest debt states. There’s a 50% overlap between states with the 10 highest credit card debt balances and the 10 highest cost of living states.

Affordable Midwest states like Iowa, Wisconsin and Idaho rank in the top five states with the lowest average credit card balances. Only three of the states with the lowest debt are among the 10 states with the lowest cost of living. This includes Iowa, Mississippi and Indiana, with Mississippi enjoying the lowest cost of living overall.

We also compared states with the highest and lowest debt totals to financial literacy rankings. There’s little overlap between financial literacy ratings and credit card debt. Just two states with low credit debt also rank highest for financial literacy.

Two states with the lowest debt balances rank among the most financially literate. Maine ranks seventh in financial literacy and ninth in lowest debt, and Iowa ranks eighth in knowledge and has the lowest credit card debt.

Alaska, Connecticut and D.C. rank in the top 10 highest debt totals and have some of the lowest financial literacy rates. Alaska ranks 47th in financial literacy, Connecticut is 44th and D.C. is 42nd. These states also rank within the highest cost of living states.

Credit Card Debt by Age

Most generations have a lower average credit card debt balance than the U.S. average of $5,525 in 2021. Generation X and baby boomers are the exceptions, exceeding the average by 30.9% and 12.7%, respectively.

These generations are also the only ones to exceed the national average of three credit cards per person.

Credit Card Debt by Age

| Generation | 2021 Debt | Number of Cards |

|---|---|---|

| Generation Z (18-23) | $2,312 | 1.7 |

| Millennials (24-39) | $4,569 | 2.7 |

| Generation X (40-55) | $7,236 | 3.3 |

| Baby boomers (56-74) | $6,230 | 3.4 |

| Silent generation (75+) | $3,821 | 2.7 |

Generation Z is just beginning to graduate from college, a time when the average American gets their first credit card. These Americans have fewer cards than older generations and the lowest debt balances at $2,312 — 58% lower than the U.S. average of $5,525 in 2021.

Generation X is enjoying their midlife years and has racked up the highest average credit card debt at $7,236. This generation also holds 3.3 credit cards on average, which is slightly higher than the U.S. average of three.

Average Credit Card Debt by Income

Unsurprisingly, higher income individuals tend to have more debt overall. Only Americans earning within the top 10% have a median debt over the national average, while Americans within the 59th percentile have less than the national average balance.

When we compare the average income per percentile group with the average amount of debt held per group, we find low-income earners have a much larger debt-to-income ratio, with their credit card debt alone accounting for 26.11% of their total income.

The amount of debt someone has compared to their income doesn’t drop below 10% until they reach the 40th percentile, earning an average of $52,145 a year in 2021.

Credit Card Debt by Income

| Income Percentile | Median Debt | Average Debt | Average Percentage of Income |

|---|---|---|---|

| <20% | $1,100 | $3,830 | 26.11% |

| 20%-39% | $1,900 | $4,650 | 11.98% |

| 40%-59% | $2,400 | $4,910 | 7.33% |

| 60%-79% | $3,600 | $6,990 | 6.45% |

| 80%-89% | $5,000 | $9,780 | 5.95% |

| 90%-100% | $6,000 | $12,600 | 4.31% |

Average Credit Card Debt by Race

When comparing credit card debt to average income, Hispanic individuals have the highest percentage of debt at 9.96%. Black Americans have the lowest percentage of debt at 8.59%, with an average balance of $3,940.

Black Americans also have the smallest debt balance, with a median debt of $1,300 and an average credit card debt 29.6% lower than the national average.

White Americans have the highest median and average debt at $3,200 and $6,940, respectively. This is 25.6% higher than the national average and accounts for 9.26% of the average income for white Americans.

Credit Card Debt by Race

| Race | Median Debt | Average Debt | Average Percentage of Income |

|---|---|---|---|

| Black | $1,300 | $3,940 | 8.59% |

| Hispanic | $1,900 | $5,510 | 9.96% |

| Other | $2,400 | $6,320 | N/A |

| White | $3,200 | $6,940 | 9.26% |

Average Credit Card Debt by Gender

Men and women have similar credit card debt balances, though men have 2% more debt. When we consider financial gaps by gender, women earned just 82.3% of a man’s average salary in 2019.

When we compare median income with credit card debt, we find that credit card debt accounts for 12.2% of a woman’s salary and 10.3% of a man’s salary.

This difference indicates that while men have a higher average credit card balance, women’s credit card debt is a larger financial burden.

Credit Card Debt by Gender

| Women | Men |

|---|---|

| $6,232 | $6,357 |

Average Credit Card Debt by Education

Higher education is often associated with increased financial literacy and higher pay. Both can impact access to adequate financial resources, and the average credit card debt reflects how individuals with less education rely on credit to get by.

While people with higher education have more debt than those without college degrees, debt-to-income comparisons show that credit card debt averages within four percentage points regardless of education.

Still, Americans with college degrees have higher average salaries that may allow them to save more and use credit less. As a result, their average debt is just 9.91% of their income.

Those who attended college but never graduated have the highest credit card debt-to-income ratio at 13.28 percent. This may be caused by the responsibility of student loan repayment without the increased salary opportunities that college graduates have.

Credit Card Debt by Education

| Education | Median Debt | Average Debt | Average Percentage of Income |

|---|---|---|---|

| No High School Diploma | $1,200 | $3,390 | 10.41% |

| High School Graduate | $2,000 | $4,940 | 11.74% |

| Some College | $2,700 | $6,210 | 13.28% |

| College Graduate | $3,600 | $7,940 | 9.91% |

College Students and Credit Card Debt

Young Americans tend to have the least amount of credit card debt of all generations, but they also tend to have less income than older generations. This means a few small purchases can become expensive financial burdens as interest payments grow month over month.

Smart spending early in life can have significant benefits for future financial health. Debt can become a cycle as monthly repayments make it difficult to save, so emergency expenses or even lifestyle costs encourage individuals to continue relying on credit.

When students cover their necessary expenses with credit cards and pay off the complete balance each month, they benefit from improved credit scores and credit card rewards without overpaying on interest.

The difference between these two scenarios is intentional spending and proper budgeting. You should know how much you can afford to spend each month and limit your credit use accordingly.

College students who have already accumulated credit card debt should prioritize repayment before they graduate and are faced with student loan repayment, too.

Credit Card Debt and Families

As Americans develop financial stability, credit cards continue to offer great benefits for strong planners. The better your credit score, the better your credit rewards and the lower your interest rate.

Credit card rewards can support large life goals like marriage and homeownership. Couples planning their wedding frequently cover costs with a credit card that offers reward miles that can pay off their honeymoon travel.

Using your card to cover monthly bills can also improve your credit score and get you approved for a lower mortgage rate.

That said, credit cards shouldn’t be relied on to cover your monthly expenses if you can avoid it. Families who need to use a credit card to make it to payday should consider how they can lower their monthly costs and invest in savings in case of an emergency and to fund retirement goals.

Credit Cards and Retirement

Excessive credit card debt can make it difficult to save for retirement as interest payments eat at your disposable income. Paying off debt frees excess income to invest in retirement or other wealth-building measures.

It also lowers your total debt, benefiting your debt-to-income ratio if your income decreases in retirement.

Those in retirement should keep existing accounts open to conserve their credit score and consider opening an additional account if they don’t have one exclusively in their name. If you’re an authorized user on your spouse’s card, you’ll lose access to the account if they die.

Additionally, credit cards can be an asset to your new lifestyle. As many retirees plan to vacation and start checking off items on their bucket list, credit cards can help cover travel costs.

What Increases Credit Card Debt?

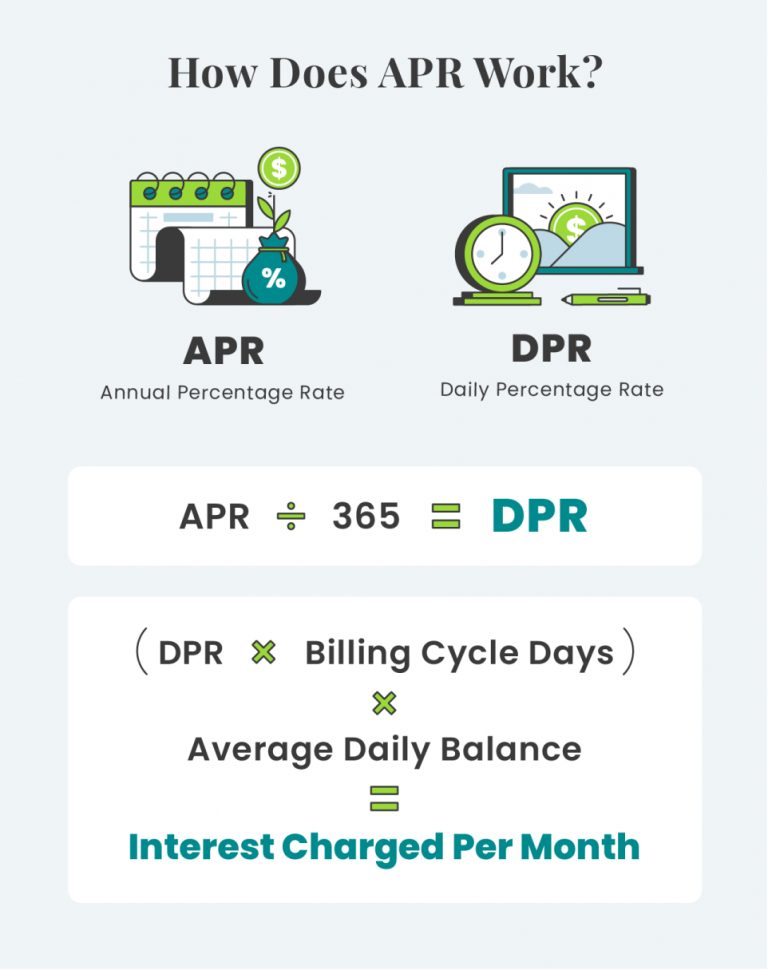

Credit card debt grows as cardholders spend more than they can afford or want to pay off each month. Leftover balances are charged interest each month according to your Annual Percentage Rate (APR).

APR is an annual interest rate, but it’s divided by the number of days in a year and applied to your average daily balance. This is then multiplied by the number of days in your monthly billing cycle.

Your lender expects a minimum monthly payment that’s either a fixed rate or a percentage of your remaining balance. Minimum monthly payments often barely cover interest charges. So if you want to get out of debt, you’ll need to pay much more than the minimum balance.

How Can I Reduce Credit Card Debt?

The best way to reduce a current debt balance is to increase your monthly payments. This helps pay off more of your balance instead of just covering interest, and reduces the interest you pay each month, too.

The snowball debt repayment method is a popular way to manage multiple accounts by paying as much as you can afford on your lowest debt balance while paying the monthly minimum on other accounts.

This lets you see your repayment progress on the lowest account, encouraging you to continue repayment until the debt is cleared — another motivator to continue maximizing repayment.

In addition to paying down existing debt, you need to adjust your finances to avoid taking on any additional debt. This includes funding an emergency savings account and creating savings goals for large purchases you’d otherwise charge to your card.

An effective budget can help you prioritize savings and track where you’re excessively spending. Once you’ve built a budget, you can confidently enroll in auto payments for your monthly expenses, knowing that the cash is available. This reduces your risk of late fees and credit penalties.

Credit cards have a bad reputation, but there are plenty of benefits for consumers of all ages who use them responsibly. The average credit card debt has decreased over the last few years, giving individuals and families the freedom to save more and stress less.

That extra spending money is also an opportunity to invest in your future with assets like annuities or mutual funds that can help you grow your wealth.