Key Takeaways

- A fixed index annuity provides a rate of return based on the performance of a market index like the S&P 500.

- You can invest your annuity premium into a single market index or across several indices.

- Fixed index annuities guarantee a minimum interest rate and you don’t lose money even if the market underperforms.

- The issuing insurance company can cap your gains to protect itself from losses.

What Is a Fixed Index Annuity?

A fixed index annuity is a financial product whose terms are defined by a contract between you and an insurance company. It features characteristics of both fixed and variable annuities.

Fixed index annuities offer a minimum guaranteed interest rate combined with an interest rate tied to a broad stock market index, such as the S&P 500 or the Dow Jones Industrial Average.

This unique hybrid design can offer protection against stock market losses, as well as the potential to profit from the market’s gains.

Fixed index annuities were created during the stock boom of the mid-1990s when investors were more interested in the potentially higher gains of stocks and less interested in stable, lower returns from investments like bonds. They were specifically designed to compete with certificates of deposit.

If you are thinking about buying a fixed index annuity, make sure you understand how growth is credited to your account. You may have a minimum guaranteed return, but your upside will be capped as well.

Brandon Renfro, Ph.D., CFP®, RICP®, EACo-Owner of Belonging Wealth ManagementAs a Certified Financial Planner™ professional and Retired Income Certified Professional®, Brandon Renfro is well-versed in the financial information and strategies needed to meet retirement goals. In addition to co-owning Belonging Wealth Management and assisting clients, Brandon writes regularly for financial publications.

How Does a Fixed Index Annuity Work?

After you sign a fixed index annuity contract, the insurance company invests your money into the market index of your choice. You can select a single index for your funds or spread your dollars across several indexes.

The most common index options include the S&P 500, the Nasdaq 100 and the Russell 2000.

In exchange for protection against losses, fixed index annuities limit how much you earn, even in strong market years.

That’s why these contracts are less risky than investing directly in the stock market, but also offer smaller potential gains.

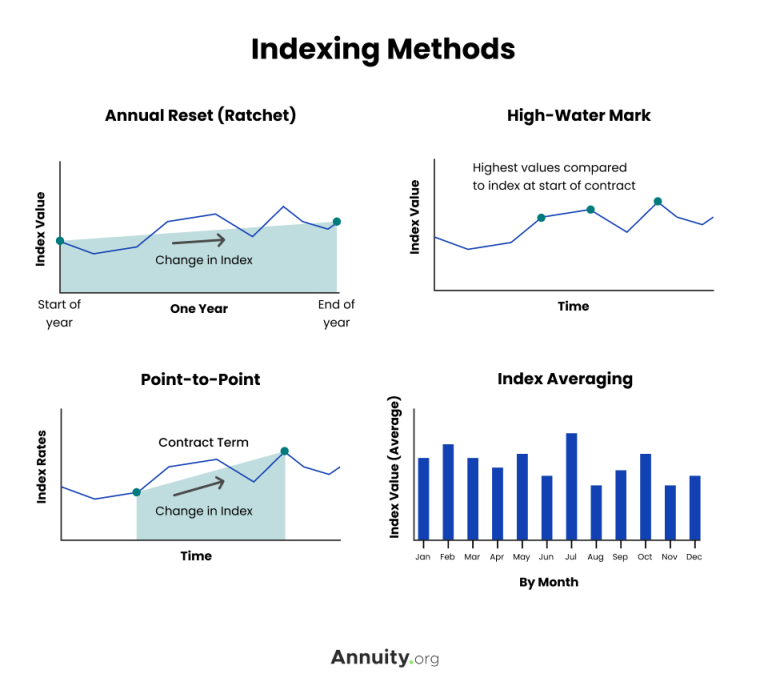

- Annual Reset (Ratchet)

- Compares the change in the index from the start of the year to the end of the year. Declines are ignored.

- High-Water Mark

- Tracks the highest point in an index’s value and uses that point as a baseline for future performance.

- Point-to-Point

- Compares change in index rates at two preselected points in time, often the start and end of the contract term.

- Index Averaging

- Averages the value of the index daily or monthly, as opposed to tracking the value on any particular date.

There are several mechanisms insurers use to determine the change in the index over the time you have the annuity:

Annuities also offer tax advantages. Interest earned within an indexed annuity is tax deferred. You won’t pay state or federal income tax on the interest until you withdraw it.

Fixed Index Annuity Yields

How your index rate is calculated will depend on the provisions of your annuity contract. According to the Financial Industry Regulatory Authority (FINRA), the computation may typically involve three factors.

- Participation Rate

- This is the percentage of the gain in the stock index you will receive on your annuity. For example, if the participation rate is 80% and the index gains 10%, the annuity would be credited with 80% of the 10% gain, or 8%.

- Spread/Margin/Asset Fee

- Some indexed annuities use this in place of or in addition to a participation rate. This is a percentage that is subtracted from any gain in the index. If the fee is 3% and the index gains 10%, then the annuity would gain 7%.

- Interest Rate Caps

- Some indexed annuities put an upper limit on your return. So if the index gained 10% and your cap was 7%, then your gain would be 7%.

Factors That Can Impact Index Rate

Guaranteed Minimum Return

Fixed index annuities carry what’s called a guaranteed minimum return. Typically, this means if you buy a fixed index annuity, you are guaranteed to receive at least a certain amount.

For example, if the stock market loses 2% of its value next year and your guaranteed minimum rate is 3%, you’ll still earn that 3%.

If your index performs consistently well, you have the potential to earn a higher return than traditional fixed annuities.

On the other hand, if the stock index underperforms, your payments will not fall below a preordained level. Guaranteed minimums on fixed index annuities typically range from 1% to 3% per year.

Read More: What Is a Fixed Annuity?

What Are the Fees and Commissions Associated With Fixed Index Annuities?

Like any other type of annuity, fixed index annuities come with fees and commissions that must be paid on top of the initial premium. The more complex an annuity is, the more expensive the fees and commissions tend to be.

Because fixed index annuities are not as simple as fixed annuities or income annuities, they tend to have higher commissions. The commission on a fixed index annuity can range from 6% to 8%, compared to the 1% to 3% commission you can expect for a fixed annuity.

Because fixed index annuities are invested in equity market indexes, there are fees associated with maintaining those investments. These include mortality expenses and investment expense ratios, which can range from 0.5% to 1.5% and from 0.6% to over 3%, respectively.

Some fixed index annuities also charge a spread fee, also known as a margin fee or asset fee, to control how much of the index’s returns are credited to the annuity. The spread fee is subtracted from the gains that the index earns. So a 4% spread fee might reduce a 12% index gain to just 8% growth credited to the annuity’s value.

Who Should Get a Fixed Index Annuity?

Fixed index annuities are best suited for investors who don’t need the money right away. According to Annuity.org expert contributor Chip Stapleton, fixed index annuities are most beneficial for investors with 10 to 15 years before they’ll need income because they’ll have time to weather any downturns that might reduce the annuity’s return.

Most fixed index annuities have some downside protection, said Stapleton, who is a FINRA Series 7 and Series 66 license holder and CFA Level II candidate.

“It might even be a floor of zero, so you’re never going to lose money,” Stapleton told Annuity.org. “But then your upside is also capped there too, so if you want to limit your bad, you also have to limit your good.”

The market exposure of indexed annuities is mediated by downside protection, meaning that these products have a moderate amount of risk. Stapleton suggested this type of annuity may be suitable for “someone who’s more risk averse but doesn’t want to avoid risk completely.”

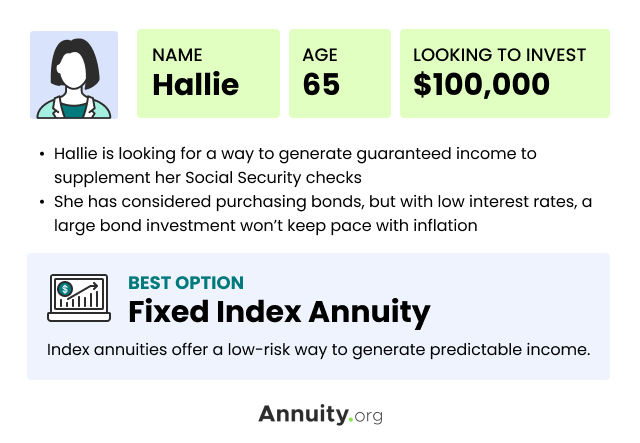

The case study below provides an example of how someone about to retire can benefit from the features of an indexed annuity.

Hallie is nearing retirement and is looking for a way to generate guaranteed income to supplement her Social Security checks.

She wants to add some flexibility to the conservative part of her portfolio. She considered purchasing bonds, but she’s worried a large bond investment won’t keep pace with inflation.

An indexed annuity is a good fit for someone like Hallie because these annuities offer a low-risk way to generate predictable income. She’s guaranteed not to lose money, so it’s a lower-risk investment than a variable annuity that would expose her to downturns in the stock market.

Some investors choose fixed index annuities over investing in index funds directly because of the associated tax advantages. Unlike traditional investment vehicles like brokerage accounts, annuities grow tax-deferred and you won’t owe taxes until you withdraw funds.

Another reason one might choose an indexed annuity is the variety of benefits and features annuities provide. Stapleton cited examples like long-term care riders, death benefits and guaranteed income as advantages that make fixed index annuities more beneficial for some people.

Fixed Index Annuity Pros and Cons

Like any investment, fixed index annuities have their benefits and costs. Since they are essentially a hybrid of fixed and variable annuities, they carry a mixture of pros and cons. They have the potential for higher returns without the risk of losing your money. Because these annuities are complicated, they can be difficult to understand.

Pros & Cons

Pros

- Tax-deferred growth

- When stocks in your index perform well, your contract value increases

- Index gains are locked in

- Principal investment protected from market downturns

- May hedge against inflation

- Rates are often better than CDs

Cons

- Gains are capped

- Lack of fee transparency

- High sales commissions

- Steep surrender charges

- Cap on increasing value may be reduced in later years of the contract

Comparing Fixed Index Annuities To Fixed and Variable Annuities

Fixed index annuities are one of the three main annuity types, along with fixed annuities and variable annuities.

Fixed annuities are not tied to the performance of the stock market. The interest rate is set in your contract at the time of purchase and does not fluctuate. The funds, therefore, are guaranteed to grow at the same rate for a specified time.

With a fixed index annuity, the number of payments to the annuity holder may increase if a predetermined stock index performs well.

The growth of variable annuities is tied to the performance of an investment portfolio. However, variable annuities don’t have the same limits on losses as fixed index annuities. If the investments you choose for your variable annuity decline, then the value of your annuity will also decline.

Variable annuities carry the risk of less growth and also offer the opportunity for more, depending on underlying investment performance.

Because the interest rate is tied to market performance, fixed index annuities expose you to more risk — and greater potential returns — than a fixed annuity. On the other hand, the guaranteed minimum return of a fixed index annuity makes it less risky than a variable annuity, but with the potential for lower returns.

“Before investing in these instruments, make sure you understand your investing horizon and think carefully about the degree to which you value safety and predictability vs. financial reward,” suggests Thomas Brock, CFA®, CPA. “To properly assess your situation, I recommend you consult with a financial advisor. He or she can help you make sense of your finances and optimize your retirement plan, thereby mitigating the possibility of outliving your savings.”

How Are Fixed Index Annuity Owners Protected?

Fixed index annuities come with a moderate level of risk due to their indirect market participation, but some protections do exist at the federal and state levels for annuity customers.

“The insurance companies that offer fixed index annuities must maintain certain standards in order to remain compliant with state and federal regulations,” Linda Chavez, founder and CEO of Seniors Life Insurance Finder, told Annuity.org. “They must adhere to a variety of consumer protections, such as disclosure requirements and financial solvency tests.”

These measures protect consumers by ensuring that the annuity provider can meet its financial obligations. The financial stability of the provider is a major factor in determining the safety of any annuity, especially those that earn a guaranteed interest rate like fixed index annuities.

“The insurance companies that offer fixed index annuities must maintain certain standards in order to remain compliant with state and federal regulations. They must adhere to a variety of consumer protections, such as disclosure requirements and financial solvency tests.”

— Linda Chavez, founder and CEO, Seniors Life Insurance Finder

The National Association of Insurance Commissioners is one organization that regulates annuity providers. The NAIC maintains a database called the Insurance Regulatory Information System (IRIS) to share data on insurers’ financial strength with state insurance departments.

When state departments are made aware of financially unstable insurance companies, they may notify the state guaranty association, the nonprofit organization that protects policyholders by paying the claims of customers when an insurer in that state becomes insolvent.

Join Thousands of Other Personal Finance Enthusiasts

Frequently Asked Questions About Fixed Index Annuities

Fixed index annuities are not securities and do not earn interest based on specific investments. Rather, indexed annuity rates fluctuate in relation to a specific index, such as the S&P 500. In contrast to variable annuities, indexed annuities are guaranteed not to lose money.

Fixed index annuities guarantee that you won’t lose money. If the index is positive, then you are credited a certain amount of interest based on your participation rate. If the market tanks, you’ll receive a fixed rate of return — or no loss of your original principal instead.

The advantages of fixed index annuities include the potential to earn more interest and the premium protection they offer. The disadvantages include higher fees and commissions and caps on gains.

A balanced retirement portfolio requires a mix of assets with varying degrees of risk. Because fixed index annuities are inherently balanced — having features of both fixed and variable annuities — these products can be included in a portfolio without skewing asset allocation.

Fixed index annuities are not as safe as fixed annuities, but they are safer than variable annuities. The guaranteed minimum return ensures that an indexed annuity’s value won’t fall below the amount specified in the contract.

An annuity rider is a contract provision that can be purchased with a fixed index annuity to mitigate undesired outcomes and enhance specific benefits.