Retirement is expensive. Experts estimate that you will need 70 to 90 percent of your preretirement income to maintain your standard of living when you stop working.

Yet Social Security benefits will replace only about 40 percent.

According to the U.S. Department of Labor, fewer than half of Americans have calculated how much they need to save for retirement. And just 44 percent of workers participate in a defined contribution plan, such as a 401(k).

These are just some of the factors that have created what many see as a pending crisis in American retirement. To give yourself an edge, start planning and saving early. Start small if necessary and increase the amount as you’re able.

When to Start Planning for Retirement

The time to start planning for retirement is now. If you are in the workforce, no matter how young, it’s never too early or too late to plan for retirement.

As you make your plans, keep these questions in mind:

- At what age do you hope to retire?

- What do you plan to do in retirement?

- How many years do you think you’ll live after you retire?

- What are your sources of retirement income?

- How long do you have to save?

- How are you going to account for risks, including inflation?

As you begin planning, you should set goals for retirement. Put them in writing and revisit them from time to time. Focus on what you can control and how much you need to save.

The planning strategies you implement depend on your career stage, your financial goals, when you would like to retire and your current financial situation. If, for example, you are a late-career professional who hasn’t saved enough to fund your retirement, you must take into consideration factors such as time horizon and risk tolerance, both of which affect the types of investments that make sense for you.

Time horizon is the period of time over which an investment takes place. Short-term investments have time horizons of fewer than three years. If you plan on retiring in 20 years, your retirement planning would have a time horizon of 20 years.

Risk tolerance refers to the level of market risk you’re willing to take. For example, stocks carry higher risks than bonds do, but stocks have more growth potential.

Making a Budget

Any retirement plan should include a budget that outlines realistic expenses and income expectations.

To start your budget, collect your last year or so of bank account and credit card statements to organize your expenses. Categorize your spending by food, clothes, housing, transportation, health care, entertainment, etc.

Don’t forget your routine costs, such as property taxes, insurance, and car registration and driver’s license renewals. Also remember nonroutine expenses such as gifts and the costs of hobbies and vacations.

- Plan for emergencies

- Incorporate some savings cushion for things like home and car repairs, unexpected medical costs and family emergencies.

- Add up your assets

- Get the most recent statements from any 401(k), IRA and other investments and savings.

- Estimate income

- If you expect to receive a pension, include that income. And you can estimate your Social Security income online. Don’t forget any annuity income.

- Remember inflation

- As you prepare your budget, consult the Bureau of Labor Statistics for current and historical inflation rates, and account for it in your projections.

- Investment earnings

- Determine the average rate of return expected on your investments.

- Use tools you’re comfortable with

- If you like writing on paper, use paper. If spreadsheets or computer documents are your thing, go that route. Don’t let the method get in the way of planning.

It’s especially important to make sure you include health care costs. If you plan to retire before you’re eligible for Medicare at age 65, make sure to include the cost of health insurance your employer will no longer be funding. Try to project other health care costs, such as copays, long-term care and dental expenses that are not covered by Medicare.

Once you have a breakdown of your expenses, identify your sources of retirement income and compare the expenses to your expected income. Review the national average retirement income to assess the health of your finances.

Can You Retire Comfortably?

Retirement Planning Tools

Take advantage of the retirement planning tools available online to prepare for your golden years. These tools can help you estimate how much you need to save, what kind of income you can expect and what resources are available to get you to a strong position.

For example, the federal government offers a retirement page on its website that includes tips about Social Security, federal and private pensions, civil service and retirement savings.

Other government-sponsored and nonprofit online retirement planning tools offer guidance on monitoring financial health, early and late retirement, retirement plan laws and maintaining your lifestyle in retirement.

FINRA

The Financial Industry Regulatory Authority is a nonprofit organization that regulates brokerage firms and the sale of securities, such as stocks and bonds. In addition, FINRA works to educate investors through a variety of resources, including retirement planning tools.

Social Security Administration

The Social Security Administration is a government program established to provide financial protection to Americans through benefits programs including retirement.

- Retirement calculator

- Life expectancy calculator

- Spousal benefits calculator

- Online benefits planner

Consumer Financial Protection Bureau

As part of its efforts to “empower, enforce, and educate,” the Consumer Financial Protection Bureau promotes financial literacy through a variety of resources, including a Social Security benefits calculator and articles about retirement payout options, pensions and debt management.

U.S. Department of Labor

The Labor Department protects the welfare of American workers and retirees. Among the department’s chief responsibilities is to educate retirement plan participants about their rights under federal law.

Saving for Retirement

As you participate in the workforce as an adult, retirement will always be on the horizon, drawing closer at each stage of your career, shortening the time horizon of your investments. This can be intimidating, especially later in your work life.

Ideally, you’ll have started planning and saving for retirement when you were young, but it’s never too late to improve your outlook for retirement. Don’t let the fact that you haven’t planned yet — or planned adequately — keep you from addressing retirement now.

As experts at the Center for Retirement Research have noted, retirement “is not a linear process. Life expenses (college, the mortgage) cost more than anticipated. And life events (divorce, illness, parents’ needs) force many to start all over again.”

The researchers also noted that pre-retirees can be immobilized by things that affect their emotions. They can become angry at their boss or the government and experience anxiety over their investment decisions.

The best way to overcome this is to focus on the things you can control. Sometimes baby steps are the only way to move forward. But as long as you are making progress, you are improving your chances of success.

Starting in Your 20s and 30s: Early-Career Planning

Your early career is the ideal time to start saving and making it a habit. Set aside a little of each paycheck before you get used to having the full amount at your disposal.

When you become financially independent, create a budget that includes retirement savings.

This is a time to become comfortable with your finances. People who are financially literate are generally better able to handle money and less likely to run into problems.

Participate in your employer’s retirement savings plan. At minimum, the automatic payroll deductions will make saving easier, but you might also receive a tax benefit from saving pretax funds. And if your employer offers matching funds, take advantage of them. Do not leave free money on the table.

This is also a good time to establish a pattern of living within your means and avoiding the temptation to buy more as you earn more. If you buy a house, for example, make sure you can afford the mortgage payments. You don’t want to be “house poor.”

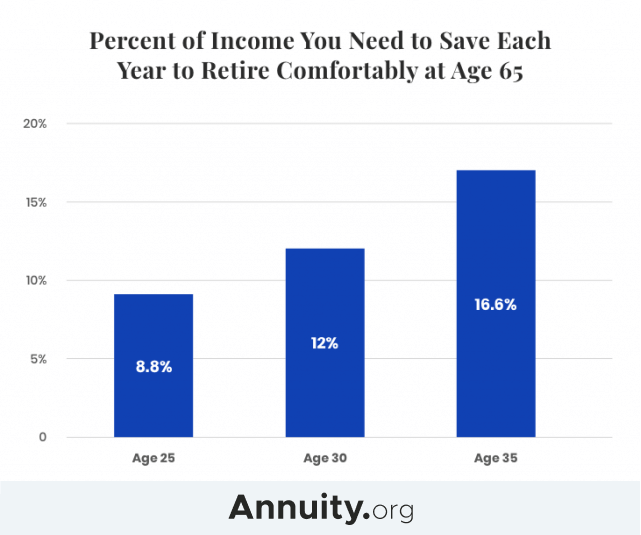

The earlier you start, the more time your savings will have to accumulate and compound. Compounding is key here. This means that your interest will earn interest and that interest will earn interest and so on with every passing year. This increases the chances of you enjoying a comfortable retirement. It also decreases the amount you will need to save every year.

Wade Pfau, professor of retirement income at the American College told Money that a worker who starts saving at age 35 will have to put away 16.6 percent of their income for 30 years to retire comfortably at age 65. If the same worker starts saving at 30, the requirement drops to 12 percent. At age 25, just 8.8 percent — including the company match — must be saved every year until age 65.

Starting in Your 40s and Early 50s: Mid-Career Planning

As you enter mid-career, keep revisiting and building on your retirement plan. Start to envision how you’d like to spend your retirement years. These tend to be your peak earning years, so do whatever you can to increase your earnings and your savings for retirement.

If you haven’t started saving, start as soon as possible. When you can, increase the amount you save. Keep track of your investments to make sure they’re allowing you to reach the goals you have set, and consult with a professional investment advisor or retirement planner to make sure you’re on track.

Look for opportunities to increase your savings. For example, when your children leave the home, your spending should decrease. Yet a study by the Center for Retirement Research found that, in spite of the fact that people at this stage of life are less likely to have mortgage payments, households increase contributions to 401(k) plans by only 0.3 to 0.7 percentage points when the kids leave home.

Now is also the time to consider the effects of committing, or recommitting, yourself to a healthy lifestyle on your health care costs in retirement. The Aegon Retirement Readiness Survey 2021 concluded that “Leading a healthy lifestyle is perhaps the best backup plan especially during a pandemic and a significant factor in preparing for a comfortable and active retirement.”

Starting in Your 50s and Early 60s: Late-Career Planning

Ideally at this point, you’ve been preparing for retirement and have saved as much as possible. For some, though, retirement seems to sneak up; other priorities have gotten in the way of retirement planning.

That’s understandable. There’s still time.

When you’re 50, you’re also allowed to make extra deposits to retirement savings plans, known as “catch-up contributions.” These contributions have the same tax advantages as your ordinary deposits.

If you’re really behind, you may have to consider working longer than you’d planned. If you stay in the workforce until age 70, you will maximize your monthly payments from Social Security. This also gives you more time to save and more time for your savings to build.

After you retire, you might consider taking a part-time job to supplement your savings.

Examine any financial help you are giving to your adult children. Try to minimize that to ensure both that they are financially independent and that you are better positioned for retirement. Forty-three percent of parents responding to a survey in 2022 reported risking their retirement security to provide financial assistance to their adult children.

Start reducing your debt. If you have a mortgage, make extra mortgage payments each month. When it’s time to retire, you can refinance your newer, smaller balance to make it more manageable on a reduced income.

If you live in a large house, consider selling it and buying something smaller and easier to maintain. Reducing your mortgage payments will allow for more cash to put into your retirement.

Take a serious look at your retirement portfolio to make sure it’s on target. Update your retirement budget and adjust your investment strategy as necessary.

Think about how you want to spend your time in retirement. Where do you want to live? Do you plan to work part-time? Do you hope to be near family? Will you travel? Do you have any hobbies? What do they cost?

Read More: Essential Retirement Statistics for 2023

Retirement Account Options

The Internal Revenue Service regulates more than a dozen kinds of retirement savings plans. Depending on your circumstances and eligibility, you may participate in any of these plans. Or, alternatively, you could purchase an annuity to provide you with a reliable income stream in retirement.

401(k)s

Many employers offer 401(k) plans as a means for employees to contribute a portion of their wages to a retirement savings account. Some employers also match a portion of the contributions.

Money contributed to a 401(k) is tax deductible, and the investments in the account are permitted to grow tax deferred. Withdrawals, however, are taxed.

As of 2023, the limit for 401(k) contributions is $22,500. At age 50 and above, you can make 401(k) catch-up contributions of up to $7,500, increasing your maximum allowed 401(k) contributions to $30,000.

Often employers will offer partial matches up to a certain amount of your paycheck. For example, you may be able to deposit 4% of your paycheck and have your employer deposit an additional 3%. Make sure you understand your employer’s matching policy and do what you can to maximize your deposits and matches.

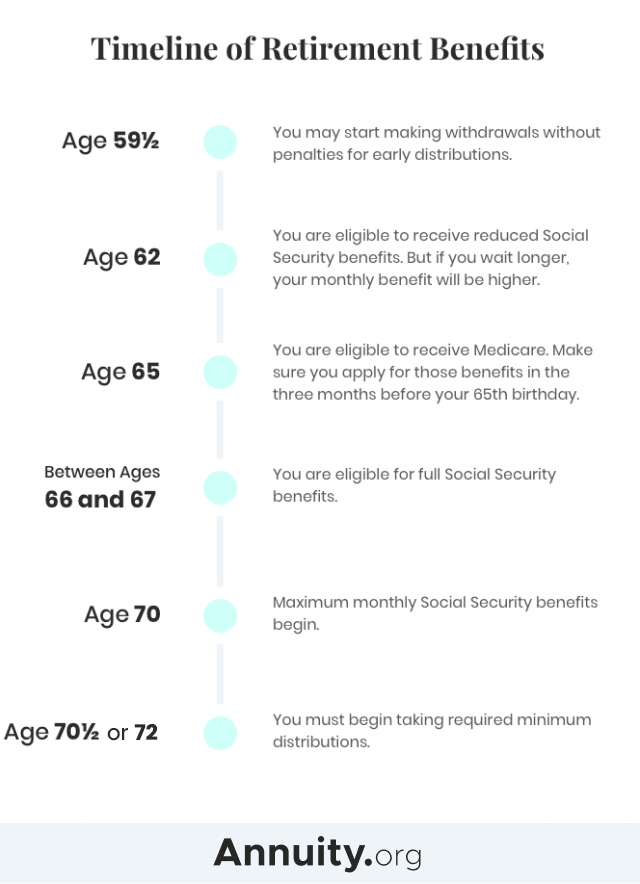

If you leave your job when you turn 55 or older, you can take penalty-free 401(k) withdrawals from the account linked to your most recent job. If you roll that money over into an IRA, you will have to wait until you’re 59½ to take withdrawals without penalty.

Traditional Individual Retirement Accounts (IRAs)

IRAs provide an easy way to save. You can set one up so that an amount is automatically deducted from your checking or savings account and deposited in the IRA. IRAs also provide tax advantages.

When you open an IRA, you have two options — a traditional IRA or a Roth IRA. The tax treatment of your contributions and withdrawals will depend on which option you select.

For example, eligible contributions to a traditional IRA are tax deductible. Roth contributions are not tax deductible.

You can put up to $6,000 a year into an IRA. If you are 50 years old or older, the limit is $7,000 a year. These limits are for the total of all your IRA accounts, both traditional and Roth.

The limits don’t apply to rollover contributions from another retirement account.

Before the law changed for 2020, you ware not permitted to make deposits into a traditional IRA after the age of 70½. And at that age, you were required to start taking withdrawals, known as required minimum distributions.

As of 2020, however, you can contribute to your IRA at any age. Required minimum distributions also don’t begin until the age of 73 under an updated new law that took effect in 2023, raising the requirement from the previous age of 72. People who reached 72 in 2022 or before must follow the previous rules and begin taking their RMDs earlier.

Under the new law, if you are still working at 73 and don’t own more than 5% of the business for which you work, you can postpone taking RMDs from your employer’s plan until you retire.

Roth IRA Accounts

Roth IRA contributions are not tax deductible. The advantage is that withdrawals are then tax-free. And you can continue to make contributions to a Roth IRA after you reach age 70 ½.

Similarly, you are not required to take withdrawals from a Roth account at any particular age.

Withdrawals from Roth accounts are not taxable if they are considered qualified distributions. To be considered a qualified distribution, the withdrawal must occur at least five years after the account was created and the first deposit was made.

Also, you must meet one of the following requirements:

- You are at least 59½ years old.

- You are disabled.

- You are the beneficiary of a Roth owner who passed away.

- The withdrawal is made by a beneficiary of your estate after your death.

- Up to $10,000 was used to buy, build or rebuild a first home for you, your spouse or your spouse’s child, grandchild, parent or other ancestor.

If you withdraw money that is not considered a qualified distribution, you may have to pay a 10% tax penalty for early withdrawals.

As you get closer to retirement, you may want to consider rolling your IRA or 401(k) over into an annuity to convert your savings into retirement income.

Can You Retire Comfortably?

Annuities

A retirement annuity allows you to create a stream of income that lasts through the remainder of your life after you retire.

Income annuities – annuities that are annuitized – provide protection against retirement risks, particularly longevity risk, which is the risk of outliving your savings. They offer the same favorable tax treatment as other retirement plans, as they grow tax deferred until funds are withdrawn.

When the SECURE Act was signed into law in 2020, Congress madee it easier for companies to include annuities in their retirement savings plans. The idea was to make defined contribution plans more like defined benefits plans. In other words, to make retirement savings plans more like pensions.

Currently, 401(k) plans can offer annuities as part of their plans. But very few companies do that, partly because of legal concerns involving the insurance companies that sell annuities. Legislation would provide protection for companies that allow annuities as part of their plans.

Self-Employed Plans

Self-employed individuals have various options for retirement savings, in addition to IRAs.

The primary account is called a Simplified Employee Pension (SEP). This allows you to contribute up to 25% of your net earnings — capped at $66,000 for 2023.

Self-employed workers can also create and invest in their own 401(k) plans and an IRA known as a Savings Incentive Match Plan for Employees, or SIMPLE IRA.

With a SIMPLE IRA, you can invest up to $15,500 of your net earnings, with no limits on the percentage of your earnings this accounts for, and either a 2% fixed contribution or a 3% matching contribution. If you are 50 years old or older at the end of the 2023 calendar year, you can add another $3,500 as a catch-up contribution.

Cognitive Decline

When you’re planning for retirement, it’s important to account for the possibility of cognitive decline in your later years. As you get older, in other words, your ability to make decisions and analyze finances may be limited by the normal aging process.

Researchers have found that financial literacy declines with age, even as confidence in financial decision-making increases. This combination, researchers say, explains some poor credit and investment choices by older people.

A study at the Center for Retirement Research found that more than half of people develop cognitive impairment by their late 80s. These researchers found that “normal cognitive aging can lead to financial mistakes because people lose much of their ‘fluid’ intelligence — the capacity to process new information — by the time they reach their 70s and 80s.”

The good news is, the researchers also wrote, “Retirees in their 70s and 80s are often just as able to pay the bills, handle debt, and maintain good credit as workers in their 50s and 60s.”

This is because people can rely on knowledge they’ve accumulated throughout their lives, as opposed to processing and learning new information. So people with experience in handling their finances are better positioned to weather financial challenges as they age, according to these researchers. Those facing more difficulties tend to be those who had lost a spouse who had handled those responsibilities.

The researchers concluded that retirees with normal cognitive aging who are financial novices may need varying degrees of help. And without access to trusted expertise, they will be at risk of serious mistakes. Those with cognitive impairment “face greater challenges,” including becoming targets for fraud and financial abuse from caregivers.

The Society of Actuaries has identified some areas of concern for people in their 80s when it comes to financial health. These include:

- Documents

- It’s important for people who will make financial decisions to have the right legal documents and authorizations. They also need to know how to find all relevant financial information, including assets. They should know, for example, about the locations of safes and safety deposit boxes.

- Charities

- Often, older people are inundated with solicitations from charities. Family members and caretakers should keep an eye out for this and help to keep this from overwhelming. It’s helpful if the retiree lets caregivers know in advance their preferences regarding charities so those wishes can be respected later should it become necessary to make decisions.

- Denial

- Seniors who suffer limitations, such as difficulty driving a vehicle, may have trouble accepting their condition and be in denial. Caregivers and family members are consequently faced with difficult situations in ensuring health and safety.

Compensating for Cognitive Decline

The Society of Actuaries suggested arrangements that offer financial and legal protection for those with dementia.

- Lifetime annuities

- The insurance company manages the money used to purchase an income annuity and makes regular payments to the annuitant, removing the need for the retiree to make investment decisions.

- Trust arrangements and power of attorney

- Having a reliable trustee or someone given the power of attorney to make legal and financial decisions when the retiree is unable can provide needed protection.

- Instructions to advisors and family members

- Clearly communicated and written instructions to people who will make decisions or provide advice can mitigate problems in the future and empower individuals to make the right choices for retirees.

- Money management services

- A professional money management service can help with bill paying and everyday money management if the retiree is unable.

Although it may be uncomfortable, consider the possibility that you may need assistance with financial responsibilities in your later years and plan accordingly. It’s always better to be safe than sorry.