Key Takeaways

- An annuity is an insurance product designed to provide consumers with guaranteed income for life.

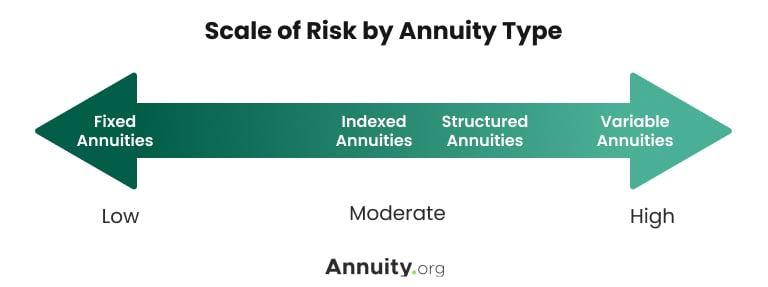

- The type of annuity you purchase determines your future annuity payments.

- The primary benefits of buying an annuity include principal protection, the potential for guaranteed lifetime income and the option to leave money to your beneficiaries. Some annuities may also be optimized to help pay for long-term care.

What Is an Annuity?

An annuityAnnuityAn insurance product that earns interest and generates periodic payments over a specified period of time, typically with the purpose of providing income in retirement. is a customizable contract issued by an insurance company that converts an investor’s premiums into a guaranteed, fixed income stream.

More specifically, an annuity contract is a legally binding, written agreement between you and the annuity provider that issues the contract. This contract transfers your longevity riskLongevity RiskLongevity risk is the risk that you will outlive your retirement savings. — the risk of you outliving your savings — to the insurance company. In exchange, you pay premiumsPremiumA regular payment made to keep insurance coverage active. as outlined in the contract.

Annuities can be a great tool to help you generate retirement income or reach other financial goals, but there are many kinds of annuities. It’s important that you understand how they work to know if one is right for you.

Brandon Renfro, Ph.D., CFP®, RICP®, EACo-Owner of Belonging Wealth ManagementAs a Certified Financial Planner™ professional and Retired Income Certified Professional®, Brandon Renfro is well-versed in the financial information and strategies needed to meet retirement goals. In addition to co-owning Belonging Wealth Management and assisting clients, Brandon writes regularly for financial publications.

Many retirees need more than Social SecuritySocial SecuritySocial Security is a federal benefits program for retirees in the United States, funded by taxes. and investment savings to provide for their daily needs. Annuities provide individuals with a way to potentially accumulate wealth, defer taxes, preserve their principal and ensure a reliable income stream in retirement.

How Do Annuities Work?

At their most basic, annuities work by converting a premium into a stream of payments. The amount and duration of the payments depend on various factors, including the type of annuity, the premium amount, the annuitant’s age and the chosen payout option.

Annuities can be optimized for income or long-term growth, but they are not short-term investment strategies. Most annuities supply income through a process of accumulationAccumulation PeriodAn accumulation period is the period of time when annuity premiums increase in value. and annuitizationAnnuitizationThe process of converting the premiums and interest earned on a deferred annuity to a stream of income through a series of periodic payments.. The exception is immediate annuities that begin paying out as soon as within a month of purchase with no accumulation phase necessary.

When you buy a deferred annuityDeferred AnnuityAn annuity contract with an accumulation phase and a payout phase. Deferred annuities begin distributing income at a specified date in the future, typically 10 to 30 years., you pay a premium to the insurance company. That initial investment grows tax-deferred throughout the accumulation phase, typically anywhere from five to 30 years based on the terms of your contract. Once the annuitization, or distribution, phase begins — again, based on the terms of your contract — you start receiving regular payments.

Annuity contracts transfer all the risk of a down market to the insurance company. This means you, the annuity owner, are protected from market risk and longevity risk. To offset this risk, insurance companies charge fees for investment management, contract ridersRiderA provision added to a contract., and other administrative services. In addition, most annuity contracts include surrender periods during which the contract holder cannot withdraw money from the annuity without incurring a surrender charge.

Furthermore, insurance companies generally impose caps, spreads and participation rates on indexed annuities, each of which can reduce your return.

Other features of annuities:

- Riders

- Death benefits

- Living benefits

- Fees and commissions

- Taxation

- Free-Look Period

Read More: What If Your Annuity Provider Changes?

Will You Be Able to Maintain Your Retirement Lifestyle?

Learn how annuities can:

✓ Help protect your savings from market volatility

✓ Guarantee income for life

✓ Safeguard your family

✓ Help you plan for long-term care

Speak with a licensed agent about top providers and how much you need to invest.

Types of Annuities

Different types of annuities exist to fit the diverse needs of the market. Your personal goals and objectives will determine the type of annuity that is right for you.

GUARANTEED INCOME

Fixed Annuities

How Are Annuity Rates Set?

Annuity rates are set differently depending on the type of annuity. For example, an issuing insurance company sets the rateAnnuity RateThe rate of growth, expressed as a percentage, set by the insurance company at the start of the annuity contract term. Depending on the type of annuity, the insurance company may guarantee the interest rate for a year or longer, or the rate may fluctuate with a stock market index. for its fixed annuities and will guarantee this rate for a defined period, usually between three and 10 years.

Rate setting is more complicated for other kinds of annuity contracts whose interest rates may vary throughout the term of the contract. A fixed index annuity, for example, has both a fixed rate and a rate tied to the growth of an equity market index. The indexed rate may be set according to several factors, including rate caps and floors, to keep it within a specified range.

How Are Annuities Taxed?

Finance professionals widely recommend annuities to their clients for their tax-deferred growth potential. Once you purchase the annuity, your investment grows tax-free for the length of the contract. You won’t owe taxes until you start receiving payments when the annuity matures.

How much of that payout is taxed depends on the type of annuity. If you own a qualified annuity, you’ll pay income taxes on the full withdrawal amount. Only the earnings are taxed on non-qualified annuity withdrawals.

You can even transfer your annuity’s value to a new annuity contract without triggering any taxation. As long as the contract’s value is transferred directly through the annuity provider (or providers) and not cashed out, you won’t be taxed on the transfer. This process is known as a 1035 exchange.

How soon are you retiring?

What is your goal for purchasing an annuity?

Select all that apply

How Do Annuities Pay Out?

Annuities can be structured for immediate or deferred payout. When considering an annuity, you must first define your financial goals and when you want to start receiving annuity payments.

If you want to begin receiving annuity payments within a year or less, you will choose an immediate annuity. Alternatively, if you’d rather set your payments to begin at some point in the future, you will purchase a deferred annuity and specify the start date in your contract.

INCOME NOW

Immediate Annuities

Read More: How Much Does A $100,000 Annuity Pay Per Month?

Annuity Fees

The fees associated with annuity contracts vary widely depending on the provider and the type of annuity. Most annuities do not charge annual fees, but build commissions into the contract.

“An annuity is a type of insurance, and the salesperson will get a commission for selling the policy,” Bill Ryze, a chartered financial consultant, told Annuity.org.

In general, the simpler an annuity contract is, the fewer fees it will carry and the lower its commission will be. Commissions typically range from 1% to 10% of the contract value and may come in the form of a one-time fee or as a recurring, “stream” commission structure.

Annuity Surrender Charges

Deferred annuities usually come with surrender charges. The surrender charge is similar to the early withdrawal penalty on a certificate of deposit (CD). Each annuity contract has a different surrender period, usually in the range of two to 10 years. If you withdraw money from an annuity during the surrender period, you’ll be charged a percentage of the annuity’s total value.

Surrender charges typically decrease the further you get into the surrender period. An annuity might charge an 8% penalty in the first and second years, a 7% penalty in the third year, a 6% penalty in the fourth year, and so on.

Variable Annuity Fees

Variable annuities tend to have the most fees. This is because variable annuities are among the most complex annuity contracts and require the insurer to manage the multiple subaccounts in which the annuity premium is invested.

Common variable annuity fees:

- Administrative fees

- Mortality and expense risk charge

- Underlying fund expenses

- Rider fees and charges

- Penalties

Source: U.S. Securities and Exchange Commission

Reasons To Buy an Annuity

People buy annuities to create long-term income. While most often considered financial solutions for older people who are close to retirement, annuities can benefit investors of any age with a variety of financial goals.

Reasons to buy an annuity include:

- Long-term security

- Tax-deferred growth

- Principal protection

- Probate-free estate distribution

- Inflation adjustments

- Death benefits for heirs

“The best reason to choose an annuity is to create peace of mind that your money will provide you with lifetime income.“

— Stephen Kates, Certified Financial Planner® professional

Income annuities are generally suitable for people who are within a year of retirement and want the security of guaranteed income, or for younger people who have inherited a large sum of money and wish to protect the windfall from poor financial management.

In contrast, deferred annuities are generally not recommended for people who have short-term financial needs or younger people with more aggressive investment strategies.

Annuity Benefits

One of the key benefits of an annuity is that it allows the investor to save money without paying taxes on the interest until a later date. Annuities have no contribution limits, unlike 401(k)s and IRAs.

Another significant benefit of annuities is the creation of a predictable income stream to fund retirement. With an annuity, you don’t have to worry about outliving your savings. This is a major advantage in the post-pension age.

Your reasons for investing in an annuity should align with your unique lifestyle and financial situation.

Tax-Deferred Growth

You save money without paying taxes on the interest until a later date.

No Contribution Limits

Unlike 401(k)s and IRAs, you set the dollar amount you invest.

Fund Your Retirement

Annuities create predictable income streams for life.

Provide for Your Family

Death benefit riders allow you to transfer your money to your loved ones.

Annuity Disadvantages

Some consumers see sacrificing liquidity in return for lifetime financial security as a disadvantage. Indeed, if your financial status or short-term goals limit the amount of cash you have on hand, an annuity is probably not the right solution for you.

Other common concerns about the structure and design of annuities include:

- Commissions and fees

- Complexity

- Conservative returns (as compared with investment products)

- Loss of potential returns from other investments

The loss of potential returns is what’s known as “opportunity cost.” People with higher risk tolerance frequently cite opportunity cost as a drawback for annuities. Younger investors with longer time horizons would most likely benefit from a more aggressive investment strategy because they have time for their money to grow and could bounce back from temporary market losses.

Older investors and retirees, on the other hand, need to assess opportunity costs as they relate to their specific circumstances. It is less likely that people in this age group would consider opportunity costs a disadvantage of an annuity.

“Like all investments, annuities are exposed to certain risks. That said, if structured properly, they can be a highly beneficial aspect of a retirement plan, providing a guaranteed stream of income in a relatively low-risk, hands-off manner,” said Thomas Brock, CFA®, CPA.

Read More: First-Time Annuity Buyers

Annuities vs. Other Fixed Income Products

Annuities are often compared to other fixed-income products, including life insurance, CDs and bonds. Let’s explore how annuities stack up to these alternatives.

Annuities vs. Life Insurance

While insurance companies issue both products, there are key differences between annuities and life insurance. The major difference is that annuities provide lifetime income for the annuitant with the option to pass on income to a beneficiary after death, while life insurance traditionally serves as a death benefit after the policyholder passes away.

Annuity contracts and life insurance policies are both tax-deferred investment products, and some life insurance policies can grow over time, as annuities do. When an annuity matures, the income is usually distributed as a series of payments on a set schedule. Life insurance benefits, on the other hand, are generally distributed in a lump sum to the beneficiary of the policy.

Both products require a premium, which is what you initially pay to purchase the annuity contract or the life insurance policy. However, the way companies determine your premium is different for these two products. Annuity premiums are calculated based on life expectancy, but life insurance premiums are determined by the mortality of the insured.

Because of their differences, a sound financial strategy could include both an annuity and a life insurance policy. Whether one or both products are right for you depends on your long-term money goals.

Annuities and CDs

Annuities and CDs are both considered very safe ways to grow your savings. Both products provide a guaranteed rate of return over a set period. Annuities and CDs also both favor protecting the investment’s principal over aggressive growth.

There are some notable differences between the two products. CDs are short-term investments offered by banks, while annuities are considered more long-term products and are issued by insurance companies. Taxation on an annuity contract doesn’t kick in until you withdraw payments, while CD interest is taxed annually.

Annuities are more customizable than CDs because you can choose the terms of the contract and add features like death benefit riders. CDs also tend to offer lower interest rates than annuities because the terms are shorter.

Choosing between an annuity and a CD comes down to how soon you expect to need the money you’re investing as principal. Annuities are preferable for long-term savings goals like retirement. CDs, however, are well suited for saving for shorter-term goals such as a house down payment.

Annuities vs. Bonds

Bonds are like annuities in that both are purchased with lump-sum payments and have an established date of maturity. A fundamental difference between annuities and bonds is that annuity contracts are somewhat negotiable, while the terms of bonds are not. You can add benefits or modify terms before you finalize an annuity contract, but a bond indenture cannot be changed.

Annuities also have the advantage of being tax-deferred, while bond income is taxable. In the long term, annuities typically show better rates of return than bonds, and annuities tend to hold their carrying value better over time. The value of bonds tends to decline when interest rates rise.

Bonds and annuities can both be important tools for growing your savings. When choosing which product is right for you, consider the risks and rewards of both financial vehicles and how they align with your own financial priorities.

Annuities in 2023

The economic climate of 2023 has made annuities attractive to consumers looking to maximize their retirement savings. The trade group LIMRA reported that annuity sales in the first quarter of 2023 totaled $92.9 billion, the highest quarterly sales ever recorded.

Todd Giesing, the assistant vice president of LIMRA’s Annuity Research division, said in a press release that “LIMRA is forecasting total annuity sales in 2023 to exceed $300 billion for the second consecutive year.”

Giesing attributed the high sales in part to the exceptional crediting rates of fixed-rate deferred annuities, which continue to outperform CD rates.

Another factor contributing to the increased popularity of annuities is the SECURE 2.0 Act, which went into effect on Jan. 1, 2023. The law opened a new door for annuities in the retirement space, allowing them to be offered as an investment option within 401(k) plans.

In addition, inflation continues to pose a major risk to retirees in 2023, but annuities present a few solutions to this problem.

First, the growth rates of annuities, even the more conservative fixed annuities, are typically higher than the returns on products like CDs or bonds.

An annuity can also be helpful for consumers looking to close the so-called retirement gap, the period in which your savings and retirement income aren’t enough to cover all your expenses. Annuities can offer guaranteed income for the lifetime of the annuitant and help supplement an existing retirement account if those savings are not enough.

One type of annuity is especially good at combating the effects of inflation. An inflation-indexed immediate annuity is tied to the movements of the Consumer Price Index, which is the index used to measure inflation. You can further customize an annuity to hedge against inflation by adding a cost-of-living adjustment rider. This feature increases the monthly payouts of the annuity to keep pace with inflation.

Is an Annuity a Good Investment?

To determine whether an annuity is a good investment, you must consider your personal investment needs and goals. It’s also important to account for factors like your age, risk tolerance and lifestyle.

The younger you are, the more risk you can typically tolerate. While you’re young, you might invest in products with greater growth potential. The returns on annuities are modest compared to stocks and other investment vehicles, but they offer guaranteed growth over an extended period.

Annuities tend to be sound investments for older consumers preparing for retirement. The modest returns annuities provide are balanced out by principal protection and tax-deferred growth. Annuities also provide a stream of income you can’t outlive, unlike other retirement solutions.

When deciding whether to invest in an annuity, weigh which characteristics of a savings vehicle are most important to you. If you want a safe investment that allows your money to grow tax-deferred and gives you the option to pass on your investment to a beneficiary, an annuity might be the right choice.

More: Immediate Annuity Calculator

How To Buy an Annuity

Annuities are issued by insurance companies, but most contracts are not sold directly to the public by the company’s own agents. Most annuities in America are purchased from distributors, brokerage firms, banks, mutual fund companies and independent agents.

These distributors will work with you to negotiate your contract and help you manage the contract as your annuity matures. You will primarily work with the agent who sold you the annuity, though you may occasionally receive information from the insurance company that backs the annuity.

Read More: The Cost of Waiting for Interest Rates to Rise

How To Stay Safe When Considering an Annuity

Annuities can be a safe and beneficial financial instrument, but their complexity means some bad actors can take advantage of the public’s lack of understanding. Unscrupulous brokers and agents sometimes target older Americans for annuity fraud and other scams.

“Like all investments, annuities are exposed to certain risks. That said, if structured properly, they can be a highly beneficial aspect of a retirement plan, providing a guaranteed stream of income in a relatively low-risk, hands-off manner.”

— Thomas Brock, CFA®, CPA

Unethical insurance agents may use high-pressure sales tactics or make outright fraudulent statements, swindling customers into purchasing products that they don’t need or that are detrimental to their financial wellness.

To avoid purchasing a product that’s not right for you, it helps to ask the right questions.

“Make sure you understand all the fees and what the total adds up to,” Kendall Meade, a Certified Financial Planner® professional at SoFi told Annuity.org. “Also, make sure you understand how long you will be locked into this product.”

A broker who dodges questions or doesn’t want to give you time to do your own research might not have your best interests at heart. Ryze said customers should be wary of any salesperson who offers a “limited-time deal” that’s shorter than the time it takes to invest.

“Any honest agent should present their deal and give you enough time to research and think it through,” said Ryze.

Ryze also pointed out some other red flags that could signal an unethical annuity salesperson. These signals include making promises about the growth of an annuity that has market exposure, insisting that you won’t be able to make any changes to the annuity contract and offering a deal that seems too good to be true.

Finally, potential customers should only purchase annuities from licensed agents or brokers.

A broker should be willing and able to produce evidence of their credentials when asked.

“Hesitance to provide credentials or inability to see the company’s track record could be a red flag,” Ryze said.

Join Thousands of Other Personal Finance Enthusiasts

Frequently Asked Questions About Annuities

All annuities share similar fees, but the total cost of an annuity can differ by type. When you purchase an annuity, you pay a premium that can be converted into a fixed income stream. The annuity’s administrative fees offset the risks held by the annuity provider, including market volatility. Your contract will outline your financial obligations and the annuity’s growth rate.

Benefits of annuities include:

- steady income

- tax advantages

- no contribution limits

- supplemental retirement income

In the event of death, annuities also offer riders that allow you to transfer money to your beneficiaries.

Purchasing an annuity is among the safest options for long-term financial planning. They are insurance products, so they experience less volatility with market fluctuations, although some annuity types have higher risks — and higher potential rewards — than others.

Annuities are insurance products, and annuity providers are often insurance companies. Although the annuity itself is not insured in the literal sense, annuity owners are protected by state guaranty associations if the insurance company defaults on payments.

You can designate one or more beneficiaries in your annuity contract if it has a death-benefit provision. The beneficiary would inherit either a specific amount or the remaining money in the annuity.

The typical age for buying an annuity is between 45 and 75, but a multi-year guaranteed annuity (MYGA) can be suitable for just about any age.

When you purchase an annuity, your premium is placed in an investment portfolio called an annuity fund. This portfolio determines the rate of return you’ll earn on your annuity.

Annuities carry certain risks, such as the risk of losing money if your annuity has market exposure. There’s also the risk of having to pay a penalty if you need to withdraw your money from the annuity early.