What Are Early Withdrawal Penalties?

When you purchase a certificate of deposit (CD), you agree to keep a certain amount of money with a financial institution to earn interest over a set period. Once your CD’s term is over, it “matures,” and you can either roll the funds over to another CD or liquidate it to receive the principal deposit and interest.

Because CDs are designed to earn interest over time, banks discourage CD holders from withdrawing money from the account before the maturity date. Almost every CD you’ll find levies some version of an early withdrawal penalty. If a CD holder needs to withdraw funds or close their CD before it matures, they won’t get all their money back, because some of it will be charged as a penalty.

How Are Early Withdrawal Penalties Determined?

How an early withdrawal penalty is determined varies by the issuing bank and the term of the CD. An early withdrawal penalty is usually calculated as the amount of interest the CD would earn over a defined period. For example, you might see the penalty described as “six months of interest” or “90 days’ interest plus accrued but uncredited interest.”

Federal law sets the minimum penalty for a withdrawal within the first six days after deposit as seven days’ simple interest, but there is no maximum penalty. If you’re considering purchasing a CD, you should always check the fine print to find out how much the penalty would be for an early withdrawal. Understanding the terms and conditions of financial products like CDs is a key tenet of financial literacy.

If the issuing bank offers multiple term options, the penalties will usually range based on the length of the CD’s term. For example, a bank might charge 60 days of interest for an early withdrawal on a 1-year CD, 120 days of interest for a 3-year CD and 150 days of interest for CDs with terms of five years or longer.

Calculating an Early Withdrawal Penalty

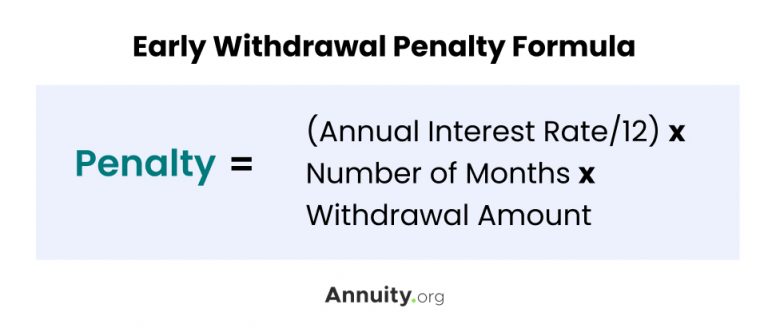

Once you know the specifics of your bank’s early withdrawal penalties, you can calculate how much it will cost you to take your money out before the contract term is over. All you have to do is multiply the monthly interest rate (the annual interest rate divided by 12) by the number of months’ interest the penalty charges, then multiply that by the amount you’re withdrawing.

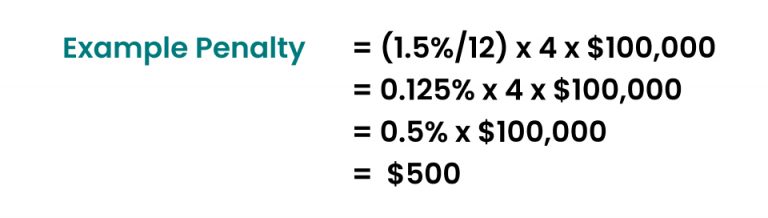

Let’s look at an example. Say you want to close a 3-year CD with a 1.5% interest rate and an early withdrawal penalty of four months’ interest. You want to withdraw the entire $100,000 amount you initially deposited in the account.

- Monthly Interest Rate

- First, determine the monthly interest rate by dividing the 1.5% APY by 12. Your monthly interest rate is 0.125%.

- Interest Penalty

- You’ll be charged four months’ interest for your early withdrawal, so multiply the monthly interest rate by four. Your penalty will be 0.5% of your withdrawal amount.

- Total Penalty Amount

- Since you’re closing the account, you’ll multiply the interest penalty by the entire $100,000 deposit. The 0.5% interest penalty means your total early withdrawal penalty will be $500.

Example Early Withdrawal Penalty Scenario

How Much Can You Withdraw From Your CD?

If you just need a portion of the money from your CD, you may be able to withdraw part of the CD instead of closing the entire account. Some banks will allow you to withdraw the accrued interest without penalty.

You may be able to withdraw some of the CD’s principal deposit if the accrued interest is not enough to cover the full withdrawal amount. If your bank allows this, your withdrawal penalty will be based only on the amount of money withdrawn. It’s important to note that some banks do not allow partial withdrawals, so check with your institution on their regulations.

When To Withdraw

Although CD holders nearly always intend to keep their CDs until they mature, there are a few instances where it may be worth it to withdraw from your CD and pay the penalty.

If you’re facing a real financial emergency and need to withdraw some money, the penalty for withdrawing from your CD might be less severe than the alternatives. For example, if the penalty amount for an early withdrawal is lower than how much you would pay in credit card interest, loan interest or other financial penalties, it might make financial sense to pay the CD withdrawal penalty.

More commonly, CD holders might consider closing an account early to take advantage of a better interest rate environment. The fixed APY CDs provide can be a benefit or a drawback depending on how interest rates trend after you purchase your CD.

When you find that rates offered by new CDs are significantly higher than the locked-in rate of a CD you hold, it may be tempting to break the current CD early and move your money to one with a higher interest rate. But first, consider how much you’ll financially benefit from the switch.

To help you decide whether to close your CD and open a new one, calculate the early withdrawal penalty for the first CD. Then, figure out how much interest you will earn with the new CD in the time between when you’d open it and when your original CD matures.

If the interest the new CD would earn you is less than the penalty would be, it makes little sense to break your current CD for the higher-paying one. If you’ll make more money from the interest in a higher-paying CD than you would lose for closing the CD, then it may be a good idea to switch and take advantage of the better APY.

Do All CDs Have Penalties?

Nearly all CDs charge penalties for early withdrawal. Exceptions to this rule are brokered CDs and no-penalty CDs.

Brokered CDs are issued by a bank but sold through a third party, usually a brokerage. These CDs tend to offer longer terms and higher interest rates than bank CDs, plus advertise no early withdrawal penalties. If you need to access the funds in your brokered CD before the term is up, you’ll sell it on the secondary market yourself instead of paying a fee to the bank.

H3: No-Penalty CDs

Consumers who desire the guaranteed returns and minimal risks of CDs while still being able to access their money on their terms may be suited for no-penalty CDs. Some banks offer this option as an alternative to traditional CDs and savings accounts. The APY of a no-penalty CD is usually lower than a traditional CD but will likely still be higher than that of a typical savings account.

Depending on the issuing institution, there may be additional restrictions on this type of CD. At some banks, for example, there may be a waiting period before you can withdraw your money, usually a few days to a week from when the CD was first funded. Some banks may not allow partial withdrawals from a no-penalty CD. This means that you may have to withdraw the entire amount — principal and interest — and close the account entirely even if you only needed to take a small portion of the money out.

Join Thousands of Other Personal Finance Enthusiasts