What Is the Home Mortgage Interest Tax Deduction?

The mortgage interest deduction lets you subtract an amount of interest you pay on your mortgage from your taxable income when you file your tax return. The deduction can save you money on your tax bill.

While there is a limit on the amount of the loan, the deduction includes interest on any loan related to building, buying or improving your primary residence. You can also claim it for rental property or second homes that you own — with some limitations.

What Are the Limits to the Mortgage Interest Deduction?

Since 1987, there have been limits placed on the amount of the mortgage for which you can claim interest deductions. The amounts have gotten smaller and smaller, with the most recent limit listed in the 2017 Tax Cuts and Jobs Act, also known as TCJA.

- Homes Sold Before Oct. 13, 1987

- Mortgages before Oct. 13, 1987 are considered grandfathered debt and there was no limit on the amount of the mortgage. If you still have a mortgage from this era, you can deduct all interest.

- Homes Sold Between Oct. 13, 1987 and Dec. 16, 2017

- If you were issued a mortgage before Dec. 16, 2017, you can deduct interest on the first $1 million of your mortgage if you file single or married, filing jointly. If you are married and filing separately, it’s limited to just the first $500,000 of your mortgage.

- Homes Sold Before Apr. 1, 2018

- Homes sold after the passage of the 2017 Tax Cuts and Jobs Act in December but before Apr. 1, 2018, may qualify for a $1 million limit on the mortgage — if you file single or married, filing jointly. If you are married and filing separately, then it’s limited to the first $500,000 of your mortgage.

You must have had a binding contract to purchase the home prior to Dec. 15, 2017, closed on the home before Jan. 1, 2018, and purchased the home before Apr. 1, 2018.

- Homes Sold on or After Apr. 1, 2018

- You can only deduct mortgage interest on the first $750,000 of your mortgage if you file single or married, filing jointly. If you are married and filing separately, then it’s limited to the first $375,000 of your mortgage.

Limits on Mortgage Interest Tax Deduction

Limits on the mortgage tax deduction have come about because of rising home prices. It was estimated that the mortgage interest deduction cost the federal government $60 billion a year in tax revenues before the 2017 tax overhaul, according to William G. Gale at the Brookings Institution.

The figure dropped to half that after the 2017 tax overhaul.

What’s Deductible and What Isn’t?

There are several types of home loans eligible for the mortgage interest tax deduction. But there are some restrictions.

Types of Loans that May Let You Claim the Mortgage Interest Tax Deduction

- Traditional mortgage

- Second mortgage

- Home refinancing loan

- Home equity loan

- Line of credit

The chief requirement for being able to deduct interest payments is that the loan was secured by your primary or secondary home for which it’s being used to buy, build or improve. You cannot claim a deduction on personal loans or loans secured by a third, fourth or other home.

How Does the Mortgage Interest Tax Deduction Work for 2023 Taxes?

The mortgage interest tax deduction can be enough to allow homeowners to itemize their deductions instead of claiming the standard deduction on their income tax return. The itemized deduction has historically been the single largest deduction for most homeowners.

However, the 2021 Tax Cuts and Jobs Act reduced the amount of the mortgage interest deduction for loans over $750,000. At the same time, the TCJA increased the standard deduction. With a lower limit on mortgage interest deductions, many homeowners are now taking the standard deduction instead.

Example of How the Mortgage Interest Deduction Works

It’s important to calculate your mortgage interest deduction and compare your itemized deductions with the standard deduction.

If your loan is under the $750,000 limit — or other limits that apply to your situation — you don’t have to do any calculations. You will be able to claim the full amount of interest you paid.

But if your loan is above the limits, you will only be able to claim a portion of your interest payments.

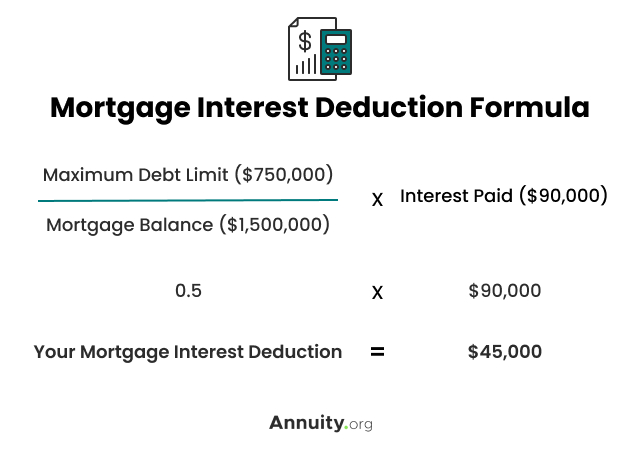

For example, let’s say you have a $1.5 million dollar mortgage — and are filing single or married, jointly — you can only claim an interest deduction based on the $750,000 limit. Let’s say you paid $90,000 in interest over the year.

You would use a formula to calculate your mortgage interest tax deduction.

In this example, you divide the loan limit ($750,000) by the balance of your mortgage ($1,500,000). This gives you 0.5, which you multiply by the total interest payments you made for the year ($90,000).

The amount you can claim as your mortgage interest tax deduction is $45,000.

How to Claim the Mortgage Interest Tax Deduction on Your Tax Return

To claim the mortgage interest tax deduction, you will need to itemize your deductions using the Schedule A (Form 1040) from the IRS in addition to the standard Form 1040.

- Schedule C (Form 1040 or 1040-SR)

- Use Schedule C if you have a home office where you conduct business or if you use money from your mortgage for business purposes. The Schedule C form covers profits and losses for self-owned businesses.

- Schedule E (Form 1040)

- Schedule E is for reporting the supplemental income you receive from real estate. Use this form to claim a mortgage interest deduction on rental properties you own.

When to Use Additional IRS Forms for Mortgage Interest Deductions

You will need to list your mortgage interest as an expense on both Schedule C and E.

Your tax forms, tax preparation software or your tax professional can walk you through the steps you need to take to claim the mortgage interest tax deduction.