Key Takeaways

- The NAIC suitability guidelines set requirements for agents and insurers to only recommend annuities that fit a consumer’s financial needs.

- Insurers and agents who adopt NAIC Model Regulation guidelines must take a four-hour educational course.

- Not all states require the mandated training from the NAIC Model regulation guidelines.

What Are the NAIC’s Suitability Guidelines?

NAIC suitability guidelines set basic standards for insurers or agents that recommend annuity products to consumers. The suitability guidelines ensures that recommended products fit consumers’ financial needs.

Suitability guidelines require the agent or insurer to gather specific information to determine a consumer’s suitability, including age, annual income, time horizon, risk tolerance and financial goals — before recommending an annuity product.

The Suitability in Annuity Transactions Model Regulation, commonly referred to as the NAIC Model Regulation, provided the framework when it was adopted in 2003, then was revised with enhanced standards in 2020.

As a consumer, you must perform your own due diligence to ensure that an annuity you choose to purchase is the best option for you. But agents and advisors that sell annuities are also required to follow certain guidelines and receive training that relate to the suitability of their recommendations.

Brandon Renfro, Ph.D., CFP®, RICP®, EACo-Owner of Belonging Wealth ManagementAs a Certified Financial Planner™ professional and Retired Income Certified Professional®, Brandon Renfro is well-versed in the financial information and strategies needed to meet retirement goals. In addition to co-owning Belonging Wealth Management and assisting clients, Brandon writes regularly for financial publications.

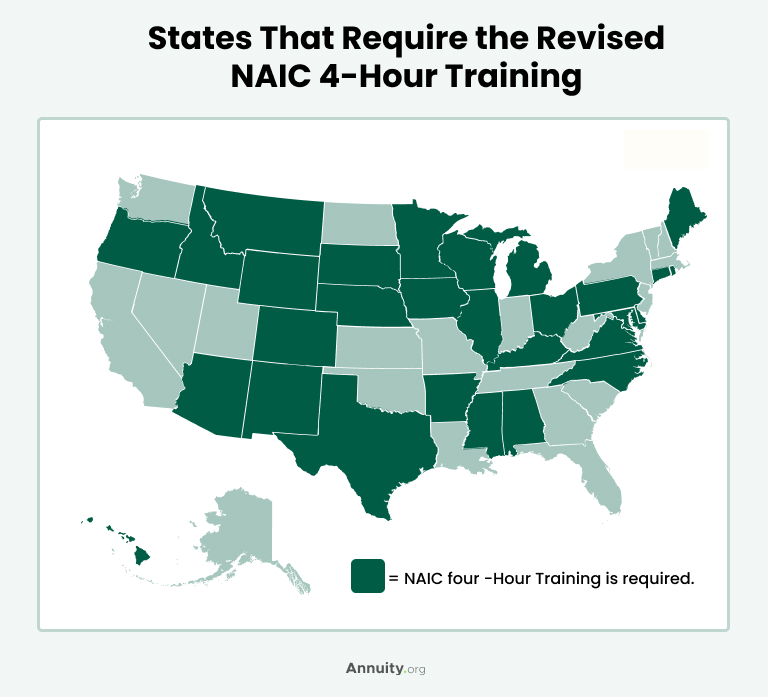

As of March 31, 2023, 34 states have adopted — or are implementing — the revisions to the NAIC Model Regulation, including the following:

- Alabama

- Alaska

- Arkansas

- Arizona

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Georgia

- Hawaii

- Idaho

- Illinois

- Iowa

- Kentucky

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Montana

- Nebraska

- New Mexico

- North Carolina

- North Dakota

- Ohio

- Pennsylvania

- Rhode Island

- South Dakota

- Tennessee

- Texas

- Virginia

- West Virginia

- Wisconsin

Source: NAIC

What Training Requirements Are Mandated by the NAIC?

Insurers or agents in states that have adopted the NAIC Model Regulation must complete a general four-hour annuity continuing education, or CE, course. The course must be administered by an educational vendor approved by the department of insurance.

The NAIC outlines training requirements for the CE course in Section 7 of its revised Model Regulation. According to the NAIC, “a producer shall not solicit the sale of an annuity product unless the producer has adequate knowledge of the product to recommend the annuity, and the producer is in compliance with the insurer’s standards for product training.”

Established agents in states that have formally adopted the revised 2020 NAIC Model Regulation will be subject to an additional one-hour supplemental course. New agents can complete a revised four-hour course that already has the updated information included in the curriculum.

The Model Regulation states that annuity-specific training includes the following information:

- Types and classifications of annuities

- Identification of the parties to an annuity

- How product-specific annuity contract features affect the consumer

- Application of income taxation of qualified and non-qualified annuities

- Primary uses of annuities

- Appropriate standard of conduct, sales practices, replacement and disclosure requirements

Are There Other Certifications Required To Sell Annuities?

Agents should be licensed in the state they sell the annuities in. The licensing process can vary by state, but most agents engage in product-specific and carrier-specific training to be knowledgeable about their business lines.

Get Your Free Guide to Annuities

What Are the Annuity Suitability Training Requirements by State?

The states that have adopted NAIC’s Model Regulation mandate the four-hour annuity suitability training, while other states have different rules in place — or no statewide requirements at all.

As a consumer, you may want to verify the level of training your insurer has completed before making your purchase.

Source: Quest CE

While most states require the revised NAIC training, some follow different training requirements.

- California:

- Eight hours of training is initially required, plus a four-hour CE training course every two years, thereafter.

- Washington D.C., Indiana, Kansas, Missouri, New Hampshire, New Jersey and Oklahoma

- The original, unrevised NAIC four-hour training is required.

- Nevada & Utah

- The original, unrevised NAIC four-hour training is required. While it is not approved yet, the revised NAIC four-hour training program is being considered. If approved, agents and insurers must complete either a new one-time, eight-hour course or an additional one-time, one-hour course within six months of the effective date.

- Vermont

- Currently, there is no annuity training requirement.

- Florida

- Three hours of training is initially required, plus a three-hour CE training course every two years, thereafter. A five-hour “Law and Ethics Update” course meets Florida’s senior suitability training requirement.

States that align with the 2020 NAIC Revised Model also designate a grace period and a deadline for existing agents to complete the one-hour supplemental training.

The following continuing education organizations provide courses that fulfill the annuity training requirements:

State requirements may change as new annuity regulations are adopted. Verify all requirements with your state or governing board.

NAIC Annuity Suitability Training Requirement FAQs

The NAIC Suitability Rule, also known as Model #275, was introduced in 2010 and set basic standards for recommending annuity products to consumers.

The NAIC’s suitability guidelines for annuities help determine if annuity products fit consumers’ financial objectives.

Per the 2023 update, 34 states adopted model revisions for annuity best interest training, according to the NAIC.