Key Takeaways

- A period certain annuity guarantees income payments for a fixed number of years, with payments going to a beneficiary if the annuitant dies before the period elapses.

- Life annuities can have a period certain option added on so that payments continue for the rest of the annuitant’s life and, potentially, to a beneficiary.

- Period certain annuities can be used strategically to fund early retirement or delay claiming Social Security benefits.

What Is a Period Certain Annuity?

Period certain annuities, also known as fixed-period annuities, pay out guaranteed income for a specified period of time — typically 10 to 20 years — regardless of whether the annuitant lives that long. Even if the annuitant dies, a period certain annuity will continue providing income payments to a beneficiary named in the contract until the specified number of years elapses.

Payments for period certain annuities are calculated to ensure that the entire value of the contract is paid out within the period. If the annuitant is still alive when the fixed period ends, the contract ceases payments.

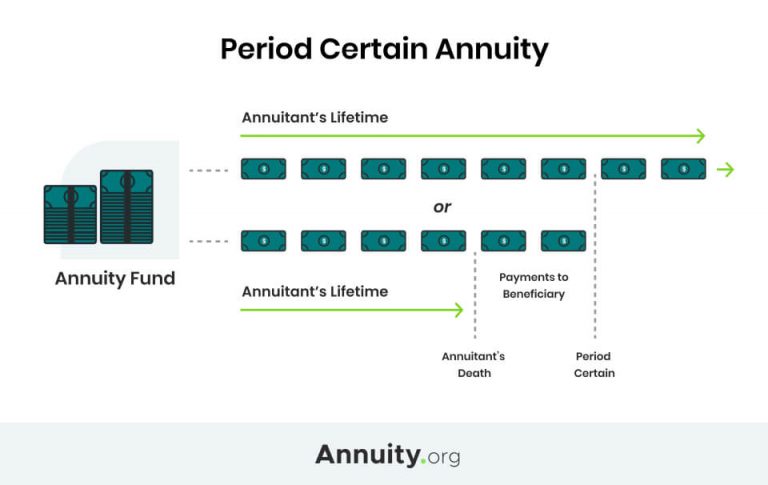

Life Annuity with Period Certain

A life annuity with period certain is a hybrid option that provides lifetime payments with guaranteed income for a specified number of years.

For example, if you purchase a single life annuity with a 20-year period certain rider and pass away 10 years later, your beneficiary will collect income benefits for another 10 years.

Without the period certain option, income benefits will be terminated upon your death. The insurance company will then apply the remaining value of your contract as mortality credits, which they will use to pay the surviving annuitants of other annuity contracts.

A period certain option added to a straight life or joint and survivor annuity means the insurance company must continue making payments after the death of the annuitant or annuitants. This means income payments will typically be lower than the periodic payments from a lifetime annuity.

“The more you’re fiddling with the guarantee to say, ‘I want more security that I’m going to get my money,’ the lower those monthly payments become,” Stephen Kates, Certified Financial PlannerTM professional, told Annuity.org. “If I say, ‘I want coverage for myself and my wife and I want it to last 30 years,’ the insurance company can say, ‘Okay, we know exactly how much we’re going to have to pay out if you live 40 years from now.’ So your payment will go down because they know how much they’re going to pay out.”

How soon are you retiring?

What is your goal for purchasing an annuity?

Select all that apply

Benefits of a Period Certain Payout

The inability to accurately estimate their return deters many people from buying annuities. This uncertainty is due to the fact that none of us knows how long we will live.

But with a period certain annuity, you know how long your payments will last. You set your payment schedule. You’ll know exactly how many payments you and your beneficiary will receive and the amount of the payments.

In addition, in instances where the period certain is less than the life expectancy of the measuring life, the payments will be larger than payments from a straight life annuity.

The defined timeframe of period certain annuities makes them ideal for bridging the gap between other sources of retirement income. For example, you might want steady income for a few years so you can retire early or delay taking Social Security payments. A period certain annuity can fit into that retirement plan, making sure you continue to receive regular income throughout your retirement.

Drawbacks of a Period Certain Payout

The period certain annuity structure guarantees income for a specific time period, regardless of whether the annuitant lives that long. This is advantageous if you die prematurely, but if you live beyond the period certain, you won’t have the security of regular income payments for the rest of your life.

Michael Kitces of Buckingham Wealth Partners emphasizes the value of mortality credits for annuity owners who live past their life expectancy and explains that “trying to protect against an annuity loss in the event of early death, and protect heirs, actually eliminates much of the benefit that annuities are meant to provide in the first place.”

This protection is the ultimate goal of a period certain annuity or a life annuity with period certain. Annuity holders who choose this payout option are choosing to forfeit the additional payments they would receive if they lived longer than other annuitants in the insurer’s pool.

Frequently Asked Questions About Period Certain Annuities

Once the specific time period defined in the annuity contract ends, payments from the annuity stop. But if you die before that time, your annuity beneficiary continues receiving the payments for the rest of the period.

For a period certain annuity, the guaranteed payout is the expected payout. Because there are a specific number of payments of a guaranteed amount, you can multiply the two together to find your exact payout.

Period certain annuities appeal to those who want both a guaranteed income stream and the peace of mind that they’ll leave the balance of their annuity to a beneficiary if they don’t outlive the contract.