What Is Longevity Risk?

From a retiree’s perspective, longevity risk is the possibility of living longer than expected and running out of money. It’s a risk that must be carefully considered during the retirement planning process. Understanding how life expectancy works can help you plan effectively.

The best retirement plans are designed to support long life expectancies and endure erratic financial markets. Moreover, they facilitate reliable streams of cash flows that keep pace with inflation. Oftentimes, these cash flows originate from qualified retirement plans, pension plans, annuities and welfare programs, such as Social Security.

Things That Impact Your Longevity

Many factors can impact your longevity. At the highest level, they can be categorized into the following buckets: genetics, lifestyle choices and environmental conditions.

Factors That Impact Longevity

| Genetics | Lifestyle | Environment |

|---|---|---|

| Gender | Diet and nutrition | Health care availability |

| Deformities | Hygiene | Communicable disease |

| Predisposition to diseases | Exercise habits | Natural disasters |

| Ability to resist diseases | Social network | Wars and conflicts |

| Education | Crime and civil unrest | |

| Occupation | Pollution levels |

There has been a long running debate over which of the categories has the most prominent influence on longevity. Some researchers assign a heavy weighting to genetics, but others believe genetics account for less than 30% of an individual’s lifespan, with the primary determinants being modifiable behaviors and environmental factors.

The findings are debatable, and new theories are continually surfacing. Nonetheless, there is little agreement on the extent to which genetics, lifestyle choices and environmental conditions influence longevity. That said, there is consensus around some things you can do to improve your chances of living a longer and healthier life.

Lifestyle Behaviors That Extend Longevity

- Avoid smoking, using harmful and addictive drugs, as well as drinking alcohol excessively.

- Eat a healthy, calorie-conscious diet and exercise regularly to strengthen and preserve your body.

- Develop and maintain a strong social network. Meaningful bonds can do wonders for a person.

- Continually stimulate your mind and pursue informal or formal educational opportunities. Ongoing learning helps sharpen cognitive health and slow the progression of decline.

- Volunteer your time and energy to help others. Doing so can have a powerful, beneficial impact on your mood and health.

How Longevity Risk Has Evolved

For most of the past century, life expectancies — and longevity risk — have been steadily increasing, largely due to elevated standards of living, advances in healthcare and medicine, and more widespread education. However, in the last few years, the trend has faltered.

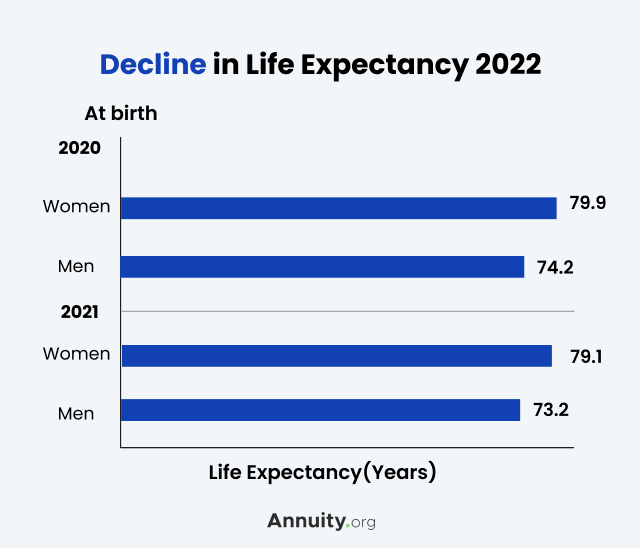

Comprehensive data hasn’t been released for the years after 2020, but projections show life expectancies have broadly declined, largely because of the COVID-19 pandemic — which disproportionately affected the elderly — and the nationwide opioid crisis. The latter resulted in an alarming impact on teens and young adults.

Based on data released in August 2022 from the Centers for Disease Control and Prevention, a baby boy born in 2021 can be expected to live, on average, 73.2 years. A baby girl can be expected to live 79.1 years.

How Does Longevity Risk Impact Your Finances?

The longer you live, the more strain you may put on your finances. This strain may be amplified when you spend more than the income generated by your savings.

If you don’t mitigate longevity risk, you could easily run out of money. This can lead to a burden on your relatives or, in the worst case, a situation where you have no financial support, beyond government welfare.

Fortunately, as outlined below, there are ways to facilitate a long, comfortable life in retirement.

How To Maximize Your Savings with Longevity in Mind

A foundational approach to extending your savings is to spend prudently. This doesn’t require you to be a miser and deprive yourself of things you value, such as traveling and spending time with your family and friends. Rather, it means maintaining a flexible budget and being thoughtful about your discretionary spending.

In tandem with a flexible budget, you could further mitigate longevity risk by employing the following tactics.

Other Ways To Mitigate Longevity Risk

- Retiring a few years later than originally planned

- Working an enjoyable, low-stress job on a part-time basis during retirement

- Downsizing to a smaller, less expensive residence and padding your savings with any gains realized

You can also combat longevity risk with specialized financial products. Three highly effective strategies that leverage these products include risk pooling in annuities, purchasing long-term care insurance and investing strategically.

1. Risk Pool in Annuities

One popular method to mitigate longevity risk is to engage in risk pooling through annuities. This entails purchasing an annuity contract from an insurance company.

In exchange for an upfront payment to the issuer, you are guaranteed a stream of future, lifetime income, combined with a pool of other independent annuity investors.

Some annuitants die earlier than expected and do not receive as many income payments as projected. The unused funds, which are referred to as mortality credits, remain in the annuity pool and are used to make payments to annuitants that live longer than expected.

In a pure risk pooling arrangement, contracts owners cannot pass unused annuity premiums to their beneficiaries. In a quasi-pooling arrangement, the option to purchase a death benefit rider could exist, depending on the issuer’s terms.

The Social Security program is often likened to an annuity because of the lifetime payments it provides to retirees. Unfortunately, for most individuals, the income isn’t adequate to meet spending needs.

2. Buy Long-Term Care Insurance

Another insurance-based way to mitigate longevity risk is to purchase a long-term care policy, which is an insurance contract that provides medical and non-medical care to an individual who is unable to perform basic daily activities, such as bathing, dressing and eating.

Policyholders can select a range of care options and benefits to obtain the appropriate services, which can be provided in a variety of settings, including personal residences, community organizations and assisted-living facilities.

Long-term care insurance can be used for individuals of any age, but it is typically purchased for older adults, oftentimes, to enhance their retirement plans. Incidentally, Medicare and most health insurance plans don’t pay for long-term care.

3. Invest Strategically

The final strategy to mitigate longevity risk is the one with the greatest upside potential — investing strategically. If done properly, this approach may do more than curb concerns about outliving your money. It could also allow you to leave an inheritance to your loved ones.

However, for this strategy to be most effective, a long runway is essential. Ideally, investing begins early in one’s working years and continues throughout retirement. The only thing that changes is the composition of the investment portfolio and the nature of fund flows.

Growth and wealth accumulation should be the focus early on in your investment journey, with a steady influx of cash bolstering your savings. Later in your journey, capital preservation and income generation take center stage as you begin drawing down on your savings.

- Early Stages

- The early-stage portfolio should be heavily allocated to publicly traded equities, with exposure to U.S. companies, as well as those based in developed international markets and emerging markets.

- Later Stages

- Over time — beginning five to 15 years prior to retirement, depending on your risk tolerance — an increasingly large portion of your portfolio should be allocated to safe-haven, income-oriented investments such as investment-grade bonds. To magnify your income potential, carving out modest allocations to floating-rate bank loans and non-investment grade bonds can be sensible.

That said, even in retirement, a meaningful allocation to equities is important. This asset class is a growth engine that can combat inflation and extend the longevity of your savings.

For most people, building an investment portfolio with fund-style investment vehicles, such as exchange-traded funds (ETFs) and mutual funds, is the optimal approach. The best fund providers offer low-cost, highly diversified access to a wide range of assets.

Unless you are an experienced investor with the ability to continually assess your tolerance for risk and run scenario-based economic projections, you should consult with a fiduciary financial advisor to optimize your retirement plan and minimize longevity risk. If you are budget-conscious and comfortable with emergent technologies, you may want to leverage a robo-advisor.