Key Takeaways:

- Generation-skipping trusts can lessen the burden of estate taxes by skipping an entire generation of beneficiaries.

- Such trusts must be assigned to a beneficiary at least 37 1/2 years younger than the creator of the trust.

- The beneficiary does not have to be a direct family member.

- For very large estates, a generation-skipping transfer tax may apply in addition to any state taxes.

What Is a Generation-Skipping Trust?

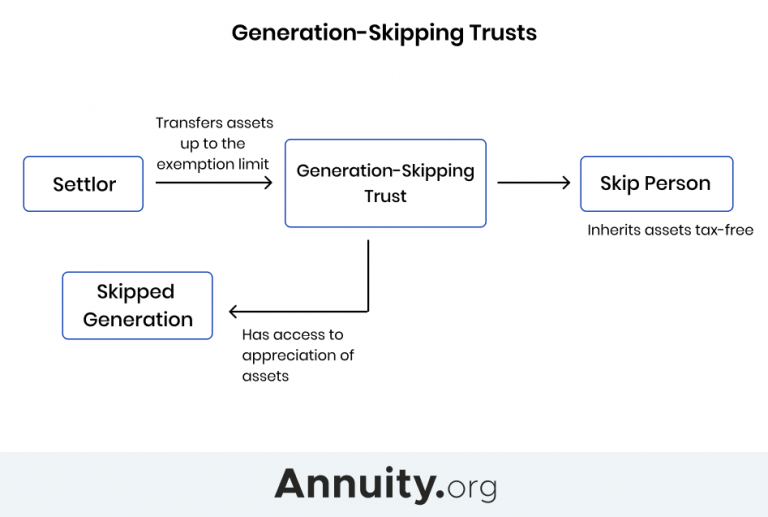

A generation-skipping trust is an irrevocable trust that assigns a beneficiary who is younger than the settlor — the person who establishes the trust — by at least 37 1/2 years. The settlor, also sometimes called a trustor or grantor, can establish a generation-skipping trust as part of a comprehensive estate plan that aims to minimize tax liability.

A generation-skipping trust is a complex legal agreement. If you intend on getting one, consider establishing this financial instrument as early as possible — ideally when you begin to plan your retirement.

At the federal level, inheritances are tax-exempt for recipients. However, the bequeathing estate may owe taxes, depending on the size of the estate. For 2023, the federal estate tax exemption is $12,060,000 and $12,920,000, respectively. Bequeathed amounts that fall below these levels are not taxable.

Thomas J. Brock, CFA®, CPAInvestment, Corporate Finance and Accounting ExpertThomas Brock, CFA®, CPA, is a financial professional with over 20 years of experience in investments, corporate finance and accounting. He currently oversees the investment operation for a $4 billion super-regional insurance carrier.

How a Generation-Skipping Trust Works

The rules for generation-skipping trust include specific parameters as to who can be appointed the beneficiary or “skip person.” According to the Internal Revenue Service, the skip person must be “a natural person assigned to a generation which is two or more generations below the generation assignment of the transferor.”

Generation-skipping trusts allow the settlor to avoid estate taxes that would be applied if the immediate next generation, meaning the children, took ownership of the assets.

If you’re considering creating a generation-skipping trust, here are some important points to consider.

First, the federal generation-skipping tax (GST) exemption amount is very high. The exemption is indexed for inflation and increased in 2023 to $12.92 million for individuals and $25.84 million for couples. You are allowed a lifetime generation-skipping tax exemption up to that amount against the property you transfer.

In addition, as long as the original assets remain in the trust for the skip person, no rule prohibits the next generation from accessing earnings on those assets.

Finally, the beneficiary does not have to be a blood relative. You can designate anyone who is at least 37 1/2 years younger than you to be the beneficiary of a generation-skipping trust, so long as that person is not a current or former spouse.

Pros and Cons of Generation-Skipping Trusts

Generation-skipping trusts are financial tools, and not every tool is appropriate for every person or situation. You’ll want to keep the potential advantages and disadvantages in mind when planning your estate.

Pros & Cons

Some of the advantages of generation-skipping trusts include:

- Ensuring your financial legacy lasts for at least the next two generations

- Reducing your estate taxes, since the assets are not directly inherited by the first generation

- Reducing potential taxes on the first generation’s estate, since the trust’s assets are never assigned as their own

- Limiting the estate’s exposure to any claims by creditors

- Not being limited to immediate family

Potential drawbacks to generation-skipping trusts include:

- For very large estates, the generation-skipping trust transfer tax may apply

- The generation being skipped might be left out if the trust is not well constructed, which can cause serious family discord

- Trusts are managed by a trustee, and the administrative burden can be costly

- The tax-filing process becomes more complicated for the beneficiary

Generation-Skipping Trust and Taxes

Although generation-skipping trusts help settlors lessen the tax burden on their beneficiaries, Congress enacted the generation-skipping transfer (GST) tax in 1976 and linked estate, gift and GST taxes into a single, unified estate and gift tax in order to close the loophole that allowed families to avoid estate taxes entirely.

As a result, generation-skipping trust distributions above the exemption threshold are subject to a 40% GST tax in addition to any state inheritance or estate taxes that may apply. In 2023, the exemption rates are $12.92 million for individuals and $25.84 million for couples.

However, if the value of the assets in the trust falls below the exemption amount, then no taxes are owed. This remains true for any appreciation of the assets, because all gains go directly to the beneficiaries. So, even if the value of the assets in the trust increases beyond the exemption limit, you will not have to pay the generation-skipping transfer tax.

RMDs: The Retirement Advantage You Can’t Afford to Miss

Estate Tax Exemption Increase

To ensure ordinary families with modest estates aren’t overly penalized, The Tax Cuts and Jobs Act enacted in 2017 doubled the estate tax exemption until the end of 2025. At that point, the exemption rate will revert to a prior amount which, when adjusted for inflation, will be somewhere near $7 million.

Such a high threshold means that most people will not have to pay the generation-skipping transfer tax. Only very wealthy beneficiaries who receive assets that exceed $12.92 million will be assessed on the taxable amount.

Gift Tax

The tax exemption of $12.92 million for individuals and $25.84 million for couples is a combined gift and estate tax exemption. That’s the amount you can gift tax-free during your lifetime or upon your death.

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.