What Is an Investment Portfolio?

An investment portfolio refers to an assortment of assets that are strategically selected by you, by an investment advisor, or by a robo-advisor to achieve your investment goals while mitigating risk. While the variety of assets you can invest in is very broad, most investment portfolios consist of some combination of stocks, bonds, alternative investments and cash.

Putting together an investment portfolio is a highly personalized process, and there’s no one-size-fits-all formula for investing. The end product should reflect your unique tolerance for risk, which will largely depend on your investment time horizon (how long you’re willing to hold the investment before cashing in) and your ability and willingness to handle fluctuations and asset price volatility in the stock market.

We’ll get into the specifics of how to go about building an investment portfolio from scratch, but for now, let’s look at the types of investment portfolios available.

Types of Investment Portfolios

At a high-level, an investment portfolio is best characterized by the degree of risk that it exhibits. Taking risk into consideration, the three primary types of investment portfolios are as follows:

Conservative Portfolio

A conservative portfolio is recommended if you have a low tolerance for risk, a short investment time horizon, or a need for a lot of liquidity. Conservative portfolios put more emphasis on capital preservation rather than capital growth. They typically consist of a large proportion of investment grade bonds, mutual funds and less volatile stocks such as large-cap stocks. As a result, conservative portfolios have relatively low levels of volatility and return potential, but they have a relatively high level of income.

Aggressive Portfolio

An aggressive portfolio is ideal if you have a high tolerance for risk, a long investment time horizon and minimal need for liquidity. Aggressive portfolios emphasize growth over capital preservation, and they usually consist of a large proportion of domestic equities (such as mid-cap stocks and small-cap stocks) and international equities in developed and emerging markets.

These portfolios tend to have high levels of volatility and return potential, but a relatively low level of income. Given their volatility, aggressive portfolios may not be a smart method of investing for beginners. As a result, some investors with aggressive portfolios choose to supplement their income streams with allocations of commercial real estate, high-yield bonds and floating-rate bank loans.

Moderate Portfolio

A moderate portfolio falls somewhere between conservative and aggressive portfolios in their level of risk. Often referred to as a “balanced portfolio,” a moderate portfolio is best if you have mixed views on risk, a long investment time horizon and a need for liquidity only from time to time. The structure of a moderate portfolio offers a balanced mix of investments focused on capital preservation, income generation and growth. Often, the starting point for this type of portfolio is a 60%/40% allocation of stocks and bonds.

Let’s Talk About Your Financial Goals.

How To Start an Investment Portfolio

Before you build an investment portfolio, you’ll need to first make sure your finances are in order. This means maintaining a sound budget, eliminating problematic debt (such as credits cards and personal loans) and creating an emergency fund with enough money to last you three to six months. Additionally, you should have a good idea of any large upcoming expenses, such as vacation plans, college tuition fees or a down payment for a home.

Once you have a good handle on your current finances, it’s time to focus on your long-term wealth goals, such as saving for retirement. Investing is a great way to put aside money for retirement, but to do it right, you’ll need to build a well-rounded investment portfolio. Seeking investment advice from a professional is always recommended, but you can also take steps on your own to build your financial portfolio.

Determine Risk Tolerance

One of the most important aspects of building an investment portfolio is determining your tolerance for risk. Your risk tolerance is a measure of your ability and willingness to accept investment losses in exchange for the potential to earn increasingly higher investment returns in the future.

Your ability to withstand the ups and downs of the stock market will largely depend on your financial flexibility, which is a product of your investment time horizon and the extend and diversity of your income streams outside of your investment portfolio. The longer you can wait to cash in on your investments, the higher your tolerance for risk.

There are additional factors at play, too, such as your psychological reaction to volatility in the stock market. You may have the time and money to handle the ups and downs of the stock market, but extreme fluctuations could feel mentally overwhelming to you. Or maybe you’re bold when it comes to investing, but if your time horizon is short and you have limited financial resources, you’ll need to take on less risk.

Evaluating your own tolerance for risk can be challenging, but it’s important to take an honest and thoughtful approach when building your investment portfolio. To guide you in your evaluation, a good first step is to take a risk tolerance quiz.

Explore Investment Account Types

As you’re starting to build an investment portfolio, you’ll want to make sure you’re opening the right type of investment account for your situation. Different types of investment accounts are used for different reasons.

Are you going to invest in an employer-sponsored retirement account, such as a 401(k) plan? Or perhaps you’re thinking about investing in an individual retirement account (IRA) or a taxable brokerage account?

If you’re fortunate enough to work for an employer that offers a 401(k) plan with a company match, this is the place to start. By investing in your employer’s 401(k) plan, you can capture the match and automatically increase the value of your portfolio. The 401(k) provider will usually have a variety of resources and tools to help you make good investment decisions.

If you can fully take advantage of the employer match and still have extra money left over, you may want to consider opening a Roth IRA account. As you work toward retirement, it’s generally recommended to have two types of retirement accounts — a traditional, tax-deferred account, and a Roth-style, tax-exempt account. Maintaining two accounts is relatively easy, and more importantly, it will enable you to have flexibility when you take income distributions in the future.

If you want to save more in your retirement accounts each year than the IRS contribution limits will allow, consider opening a taxable brokerage account where you can invest the excess.

All types of investment accounts have different tax implications, so you’ll want to do some preliminary research or ask a tax professional before you open one or transfer any money into the account.

Select Investment Types

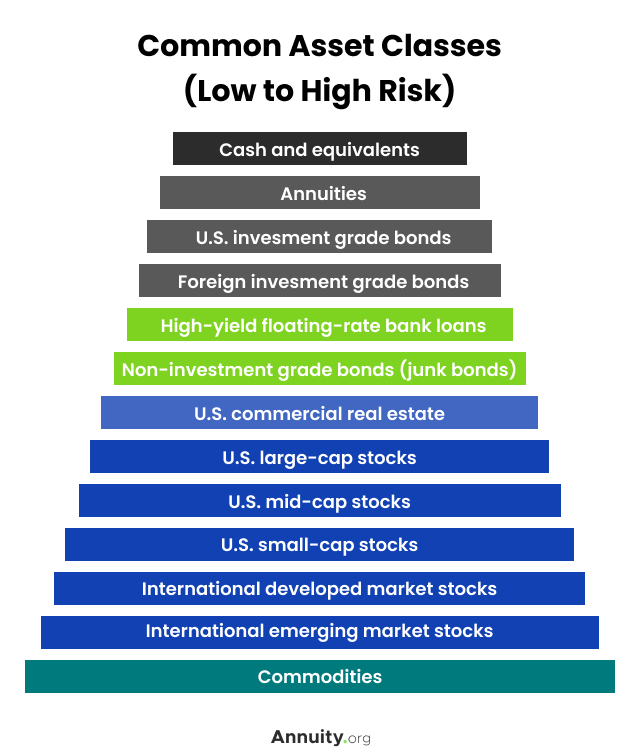

There are many types of assets that you can invest in, including stocks, bonds, floating-rate bank loans, commercial real estate, commodities, annuities and cash. The assets you pick will depend on your financial goals and your tolerance for risk.

The riskiness of these various assets is generally defined in terms of their price volatility. Cash and cash equivalents are considered the asset class with the least amount of risk (and the least volatility in price), while commodities have the highest risk and are considered the most volatile. The chart below illustrates this concept.

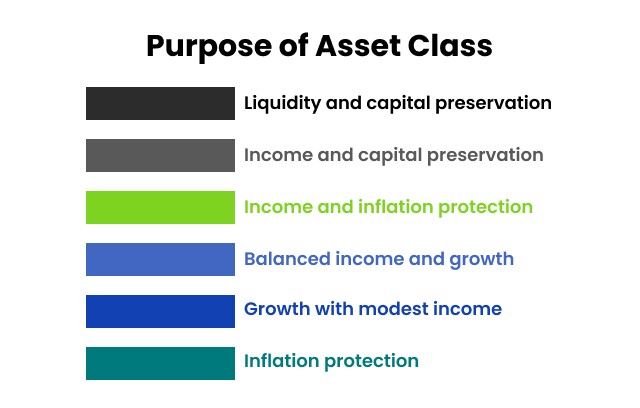

A variety of fixed-income and growth-oriented assets lie in between the two extremes, as illustrated in the chart. Each asset class serves a purpose in a financial portfolio, from inflation protection to capital preservation.

It’s important to note that high-net-worth individuals have access to other investments besides the ones we’ve already discussed, such as private equity, private credit and an array of hedge funds. Generally, these investments sit at the higher end of the risk spectrum.

Allocate Assets

After you determine your risk tolerance profile, it’s time to establish a strategic asset allocation (SAA). Essentially, this is how you specify which types of assets you’ll invest in, and how much of each asset you’ll own. Your SAA largely depends on your risk profile, but it’s also influenced by your investment objectives. Your investment goals may include some combination of capital preservation, income generation, growth and liquidity. As you determine how much of each asset you’ll invest in, understanding the concept of portfolio diversification is key.

The idea is to invest in assets that do not exhibit the exact same risk profiles. When one asset zigs, the others should zag. A diversified portfolio will maintain higher values than an undiversified portfolio, enabling you to achieve better results in the long run.

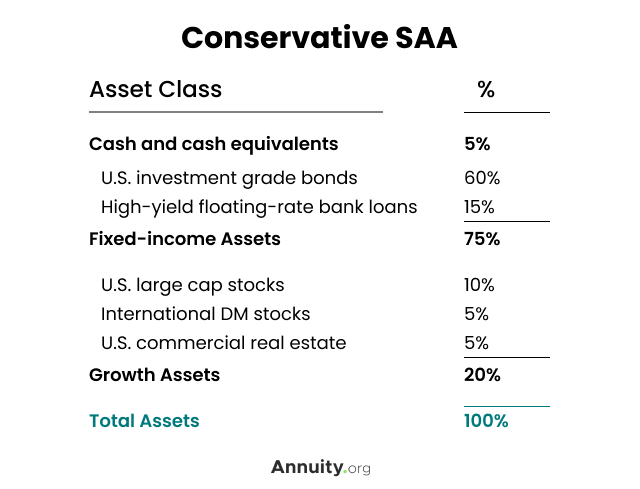

The conservative SAA is anchored by a 60% allocation of high-quality, investment grade bonds. This, along with a 5% allocation to cash, gives the portfolio a high degree of stability and a decidedly income-oriented tilt. A 15% allocation to floating-rate bank loans provides yield enhancement and good protection against rising interest rates. Finally, the collective 20% allocation to large stocks and commercial real estate gives the portfolio meaningful growth potential, with the added benefit of relatively high dividends.

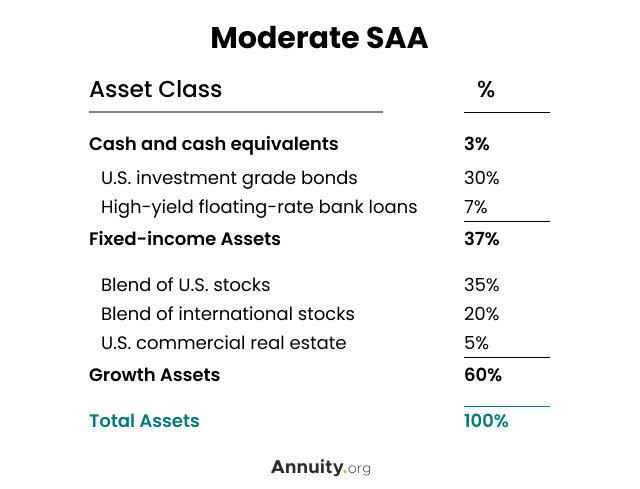

The moderate SAA is similar to a conventional “balanced portfolio” that calls for a 60%/40% split between stocks and bonds. However, this particular sample portfolio reflects a 3% allocation to cash and the inclusion of yield-enhancing, floating-rate bank loans and commercial real estate. This higher level of diversification positions the portfolio to fare better over a broader range of market environments.

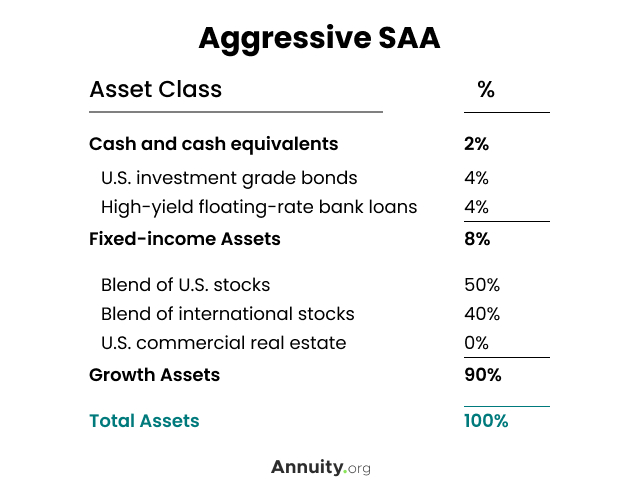

The aggressive SAA is very different from a conservative or moderate SAA. It is unquestionably growth-oriented, with a 90% allocation of global stocks. It maintains modest allocations to non-investment grade bonds and floating-rate banks loans to enhance yield and capture some diversification benefit. The 2% allocation to cash is for unexpected liquidity needs.

Once you’ve established a SAA, it’s time to actualize it by buying the specified proportions of the various assets. This doesn’t have to be overly complicated. In fact, with some basic research, you can construct your portfolio in a very low-cost and passively managed manner using a few index mutual funds or exchange-traded funds.

These fund-style vehicles, which are offered by some of the largest, most reputable investment companies in the world, provide highly diversified exposure to just about any asset or group of assets. They are economical, highly liquid and fairly easy to understand, because they track well-known indices, such as the S&P 500 Index and the Bloomberg Barclays U.S. Aggregate Bond Index.

Create Your Investment Account

When it comes time to open your investment account, you’ll need to decide how much assistance and guidance you’ll require. This will help you decide whether to go with a self-directed IRA or an account directed by a professional.

First, take a look at your financial situation and gauge your own investment knowledge and experience. Do you understand your financial situation? Can you create a long-term plan on your own? Are you comfortable making investment decisions, or do you require guidance and ongoing support?

If you’re a do-it-yourself type of investor — with clear investment goals and a good understanding of your time horizon and tolerance for risk — an online discount brokerage account is probably the way to go.

If you’ll want some help creating and maintaining a portfolio, an automated robo-advisor can be a cost-effective solution.

And if you think you’ll need hands-on, full-service help from a human and highly customized offerings, consider choosing a good financial advisor.

Things To Keep in Mind When Building Your Investment Portfolio

Once your investment portfolio is in place, don’t set it and forget it. Be diligent about monitoring your accounts and rebalancing your investments back to your strategic asset allocation, usually on a semiannual or annual basis.

If you invest in a target date fund, there is no need to do any rebalancing. The fund will dynamically adjust itself over time. Common for retirement accounts, these types of funds give you the ability to select a custom fund based on the date you plan to start accessing your money. Once selected, the administration of your investments becomes automatic, as the appropriate mix of stocks, bonds and other investments is dynamically adjusted over time.

Rebalancing is also unnecessary when working with a robo-advisor or a full-service financial advisor. This task is part of their service offering and will be completed automatically based on the terms established at the onset of your relationship.