Regardless of the stage of your life or career, you’re likely to have concerns about your taxes and you may be interested in ways to manage your tax obligations. Understanding how tax deferral can boost your retirement savings is a good start to developing a tax strategy as part of an overall financial plan.

What Is Tax Deferral?

Deferring taxes is a strategy for delaying when taxes are due and potentially keeping more money in your pocket, at least for now.

Many types of qualified retirement plans allow individual taxpayers to defer taxes on contributions and earnings. Qualified annuities also provide the benefit of delaying taxes. Taxpayers won’t owe taxes on contributions and earnings until they withdraw the money or receive income. For many, tax deferral can be a powerful incentive for people to include these tax-favored vehicles as part of their retiremen plans.

Long-term savings products, such as annuities with lengthy accumulation periods, maximize the benefits of tax deferral. The longer time horizons allow for interest to compound, so the contract owner not only saves more in taxes but also accumulates more by earning interest on interest — all with no taxes due until they receive income payments.

The IRS taxes the income benefits from annuities and retirement plans accordingly in the year during which the taxpayer receives them.

It’s important to note that “tax-deferred” does not mean “tax-free”. Understanding how tax deferral impacts your financial portfolio can help you maximize your savings.

What Are the Benefits of Tax Deferral?

The primary benefit of tax deferral is the growth achieved through compounding interest, as mentioned above. As opposed to money market mutual funds, brokerage accounts and similar financial instruments on which you pay an annual tax on earnings, tax-deferred products allow the full earned interest to remain in the account and continue to earn interest. In turn, that interest is not taxed until you take distributions. This means that tax-deferred compound interest can increase the value of an annuity or retirement plan significantly over time.

Another benefit of tax-deferred accounts is the ability to postpone taxes until you’re in a lower marginal tax bracket. Consider that it’s likely that you’ll be in a lower tax bracket during retirement years when you have less taxable income and a higher standard deduction than you had during your working years.

The Social Security Administration says that you will only owe federal income tax on your Social Security benefits if you have other substantial income (like wages, interest, dividends and other taxable income) besides your benefits to report. If your marginal tax rate is lower during retirement than when you’re working, you can shift income from your earning years (when your tax rate is higher) to your retirement years (when your tax rate is lower). Using tax planning in this way allows you to pay less in taxes overall.

Tax deferral is a powerful tax advantage that enables an individual to postpone the payment of taxes, thereby enabling him or her to accumulate pre-tax wealth more quickly. Tax exemption is an even more powerful tax advantage that enables an individual to completely avoid a tax liability.

Thomas J. Brock, CFA®, CPAInvestment, Corporate Finance and Accounting ExpertThomas Brock, CFA®, CPA, is a financial professional with over 20 years of experience in investments, corporate finance and accounting. He currently oversees the investment operation for a $4 billion super-regional insurance carrier.

Types of Tax-Deferred Products & Retirement Accounts

The IRS has varying rules for different tax-deferred products, but you can create a proactive savings strategy by understanding your tax responsibilities.

Your employment status, financial goals, investment portfolio and level of financial literacy all play a role in determining which type of tax-deferred retirement plan you are eligible for or which type of annuity you should purchase.

For example, a 35-year-old man may work for a business that does not offer a 401(k) plan, so he may choose to contribute to an IRA to achieve his financial goals. A self-employed woman who meets the criteria for establishing a SEP IRA may find the annual contribution limits too restrictive and opt instead to purchase a $100,000 annuity.

Annuities

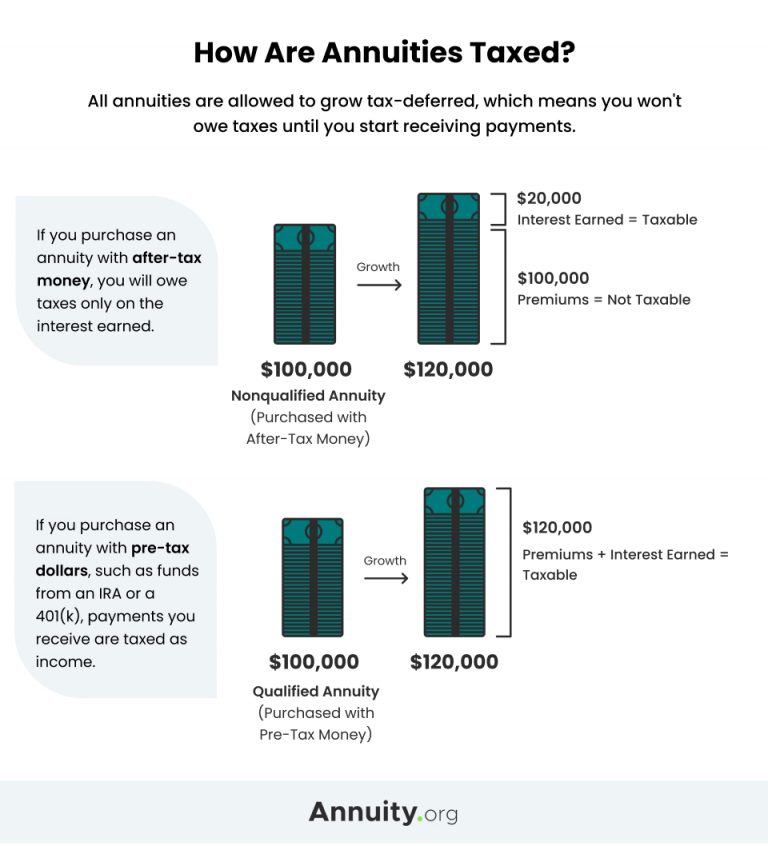

Annuities are tax-deferred risk-transfer products that can provide the contract owner with a guaranteed income stream in retirement. You can purchase annuities with either pre-tax or after-tax dollars, and the IRS treats the taxable portions of any distributions as ordinary income, not capital gains.

Tax deferral applies to the premiums and earnings on qualified annuities because you purchase them with pre-tax dollars. The same is true for qualified retirement plans, to which employees (and sometimes employers) contribute pre-tax funds. Tax deferral for nonqualified annuities, which are purchased with after-tax funds, applies only to the earnings when the annuity holder receives payments.

The IRS calculates the taxes on distributions from qualified annuities using the exclusion ratio. Also known as “the general rule,” the exclusion ratio ensures that only the taxable portion of the payments is included in the annuity owner’s gross income for the year.

How soon are you retiring?

What is your goal for purchasing an annuity?

Select all that apply

Employer-Sponsored Retirement Plans

Employers often provide defined contribution plans and defined benefit plans as retirement savings options. It is important for employees to take retirement-related benefits into consideration when they evaluate one employer’s full compensation package over another’s. Not only are there differences in plans, but some employers may contribute more than others. And yet others offer no retirement plan at all.

- 401(k) Plan

- Funded by pre-tax payroll deductions, 401(k) plans can include contributions, or matching, from an employer in the for-profit sector.

- 403(b) Plan

- Funded by pre-tax payroll deductions, 403(b) plans can include contributions, or matching, from nonprofit employers.

- 457 Plan

- Local and state government agencies and some nonprofit organizations offer 457 plans.

- SEP IRA

- Self-employed taxpayers and small businesses may establish SEP IRA plans.

- SIMPLE IRA

- Employers with fewer than 100 employees may offer SIMPLE IRA plans.

- Pension

- Pensions are employer-specified and provided retirement income, often without employee contributions.

Types of Employer-Sponsored Retirement Plans

Source: Internal Revenue Service

Regardless of the type of retirement plan offered, it’s always advisable to contribute the maximum amount that qualifies you for any employer match. The tax benefits are even greater if you’re able to contribute the annual maximum amount to your plan, which typically increases each year. And if you’re 50 or older, you can make catch-up contributions that allow you to save even more on a tax-deferred basis.

You might consider working with a financial professional who can help you develop a strategy for allocating your assets and maximizing your savings.

Individual Retirement Accounts

As an alternative or in addition to contributing to an employer-sponsored retirement plan, you can set up an individual retirement account (IRA). Depending on the type of IRA, your funds may grow tax-deferred or tax-free.

Traditional IRAs allow you to contribute pre-tax dollars, or income that has not yet been taxed. Contributions and earnings grow tax-deferred, so they are taxable only in the year they are withdrawn.

Roth IRAs are a popular savings option even though they are not considered tax-deferred accounts. Contributions to Roth IRAs are made with after-tax funds, and earnings grow tax-free rather than tax-deferred. This means that qualified distributions, including earnings you withdraw that meet IRS requirements, are not taxed as income after retirement. And because you make contributions to a Roth IRA after taxes, you can usually withdraw them at any time without incurring taxes.

The IRS mandates limits on contributions for both traditional and Roth IRAs, and a 10% penalty may apply if you withdraw funds from either type of account before you turn 59 ½ years old unless you qualify for an exception to the penalty.

While retirement accounts such as IRAs and 401(k)s provide tax-deferred growth, they come with annual contribution limits. In contrast, annuities don’t have these limits, allowing you to potentially save more money compared to the other plans.

Health Savings Accounts

Health savings accounts (HSAs) are not tax-deferred, but they offer unique advantages over other types of savings plans. HSAs allow you to set aside pre-tax dollars to be used for qualified health-related expenses either right away or in the future, which may help lower your overall health care costs.

For example, if you contribute $50 per paycheck directly to an HSA, you will not have to pay income taxes on that $50. The balance in the HSA will continue to grow without taxation, while your taxable income will decrease by $50 each paycheck. And the IRS will not tax withdrawals to pay for qualified expenses.

Saving money on income taxes now can allow you to save more for retirement. Effective planning and leveraging opportunities to defer taxes can lessen the burden of what FINRA says can be “your single largest expense in retirement.”

Although tax deferral does not eliminate your tax liability, tax-deferred options can help you save — and earn — more per dollar until you are ready to withdraw money from the account.