Analysts and investors use the yield curve to help them make more informed decisions about the portfolios they manage. The yield curve also has an important effect on annuities.

What Is Yield?

Yield is the output something generates. For investments, it is the percentage return provided by a dividend or interest payment.

There are two ways to express yield:

- Current Yield

- Yield to Maturity

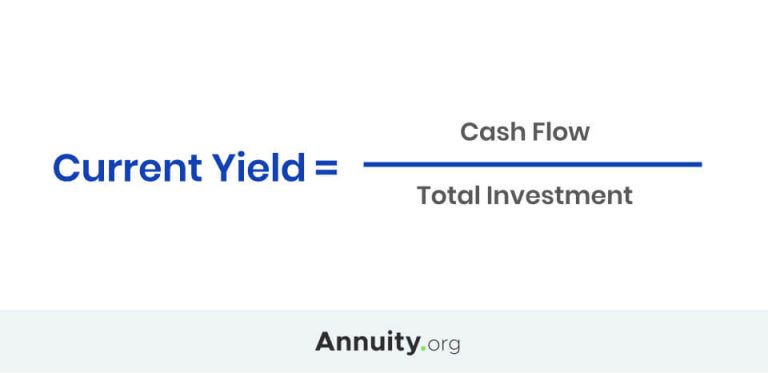

Current yield is a simple measure of the return on an investment’s cash flow represented as a percentage. The calculation for current yield is straightforward, and the formula can be applied to any type of investment — a stock, a bond, a piece of income-producing real estate or an annuity.

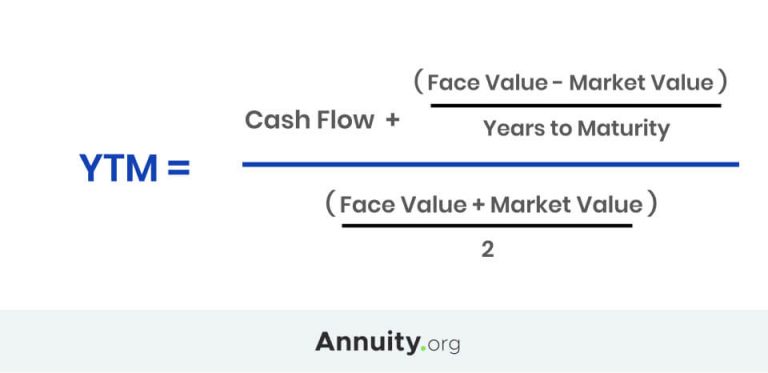

Yield to maturity is more complicated. Rather than expressing cash flow return, yield to maturity represents the actual rate of return of a bond based on its market price assuming that it is held until maturity.

The difference between current yield and yield to maturity is that current yield doesn’t account for the time value of money, which is the principle that money received in the future is worth less than money received today.

What Is the Yield Curve?

A yield curve is a snapshot of current market conditions for income-producing investments. It shows what bonds of different maturities are yielding today. And there isn’t just one yield curve. One can be created for any credit market.

For example, unique yield curves can be created for U.S. treasuries, investment-grade corporate bonds, municipal bonds, or junk bonds. One can even create a yield curve for annuities.

The yield curve is useful at showing investors the difference, referred to as the “spread,” in yield between short-term bonds and long-term bonds. The most common spread is the two-ten spread. This is the yield difference between treasuries maturing in two years and those maturing in ten years.

The two-ten spread can tell investors a lot about the business cycle and the potential direction of the economy. Yield curves can also reveal how the market feels about risk, which can be another leading economic indicator.

Comparing yield curves between bonds of different quality can show how much extra yield investors demand for taking on additional risk. For example, a wide spread between junk bonds and investment-grade corporate bonds suggests that investors are less comfortable with their risk. A narrow spread suggests that investors are more willing to take the additional risk.

A wide spread indicates that investors are concerned about future economic conditions. A narrow spread points to a more bullish economic outlook.

Yield Curve Charts to Gauge Future Economic Conditions

The shape of the curve changes over time and lends insight into potential economic conditions.

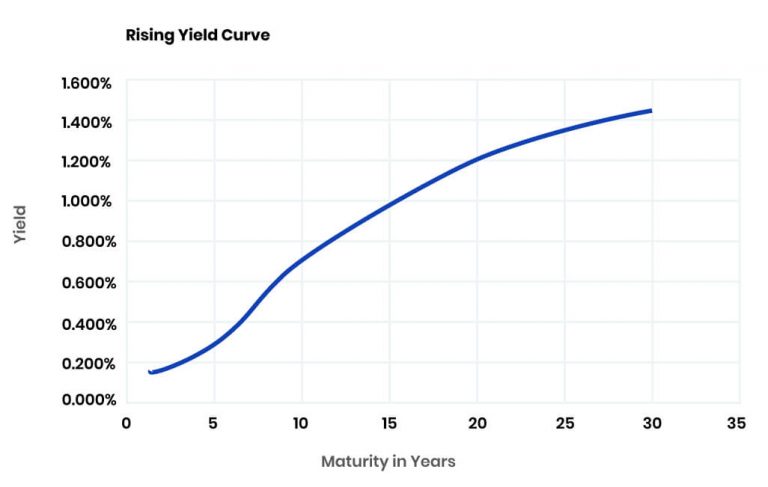

Rising Yield Curve

For example a rising yield curve often suggests that the economy will be positive in the next 12 to 24 months.

The rationale behind this is that low short-term interest rates encourage lending. By charging borrowers at long-term interest rates and paying interest to depositors at the lower short-term interest rates, banks earn the spread — or difference — between the interest they pay depositors and the interest they collect from borrowers.

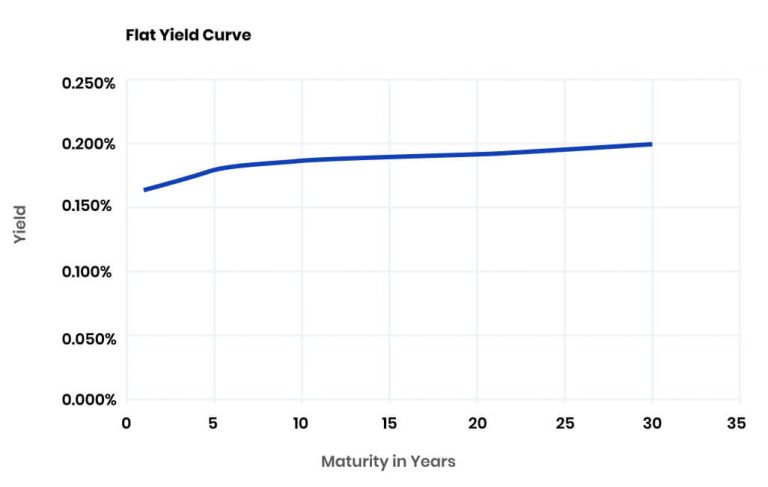

Flat Yield Curve

Because a flat yield curve neither encourages nor discourages lending, it often suggests uncertainty about the future of the economy.

Banks can’t earn a big spread when the yield curve is flat, so they approach lending more cautiously. Many view this as a precursor to recession. But it is equally likely to suggest a breather before the next period of upward movement in economic activity.

Inverted Yield Curve

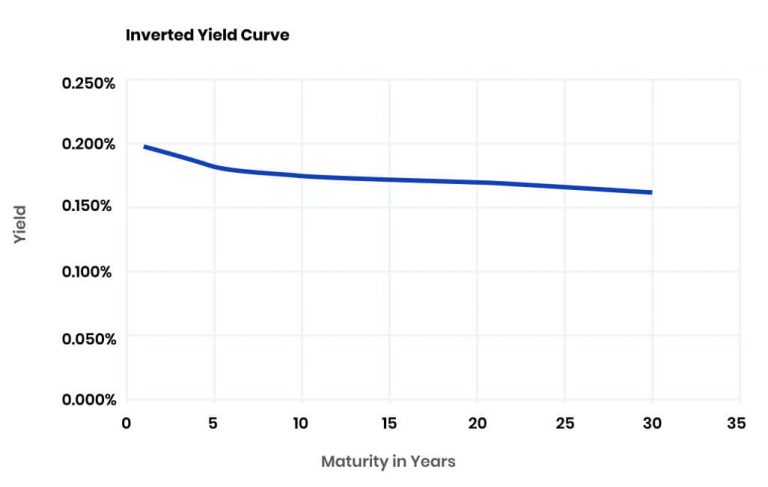

Many analysts and investors believe that a downward-sloping curve, called an inverted yield curve predicts recession. And history lends some support for this notion. Every recession the United States has experienced since the 1950s has been preceded by an inverted yield curve. But it’s not a perfect predictor.

In 1965 the yield curve inverted just before U.S. gross domestic product (GDP) rose 6.5 percent. That expansion continued into 1966, when the economy advanced an additional 6.6 percent. A similar situation occurred in 1998. The yield curve inverted briefly before the economy advanced 5.8 percent. Then in 1999, the GDP grew another 10.2 percent.

Why Interest Rates Matter to Investors

While the yield curve can be a helpful predictive indicator, what is more important in the context of long-term financial planning is how changes in interest rates might affect one’s investments. Bonds move in inverse relation to interest rates.

If interest rates rise, bond prices will fall. When interest rates decline, bond prices rise. While bonds held to term will always return their face value, those sold prior to maturity expose an investor to the potential risk of loss.

An individual investor seeking to create retirement income might choose to use bonds. Those concerned about their market value need to understand that as interest rates change, so will the value of their holdings. People who buy annuities don’t have this risk.

At any given moment, both newly issued bonds and new annuity contracts will offer interest rates that take their cue from their respective plot on the yield curve. The difference is that fixed annuities are not securities, so they are not subject to market fluctuations the way bonds are. Note that variable annuities, on the other hand, are securities and will lose value if the market declines.

More importantly, annuity payouts are typically higher than bond payouts. This is because they are less liquid than bonds — the tradeoff for the higher rate — and because, in the case of nonqualified annuities, only a portion of annuity distributions are taxable.

Still annuities aren’t the right choice for everyone. They will offer a slightly higher payout, but their rates will be very closely pegged to what the current yield curve is offering for fixed income securities of equal quality.

Purchase an Annuity Today

Should Investors Be Concerned About the Yield Curve?

Wall Street uses many sophisticated tools to guide decisions. Yet, as a practical matter, the slope of the yield curve shouldn’t be a big concern to individual investors regarding their long-term financial planning.

The reason for this is that the credit market — like the stock market — is constantly changing. And making decisions based on a belief that one can predict those changes isn’t practical. It makes more sense to consider one’s goals than to ruminate over a possible change in interest rates.

A better strategy would be to consider the role annuities can play in creating retirement income and include them to fill gaps or optimize Social Security benefits. Laddering can yield a blended rate of return to accomplish future goals regardless of what the yield curve looks like today.