Key Takeaways

- SMAs allow you to sell future annuity payments in exchange for an immediate cash payment at a discounted rate.

- Selling and buying an SMA comes with different risks and benefits. Consult with a financial advisor to determine if either is a good option for you.

- The secondary market is projected to grow in years to come.

- The annuity selling process varies depending on the type you have. For example, selling structured settlements on the secondary annuity market requires court approval.

How Secondary Market Annuities Work

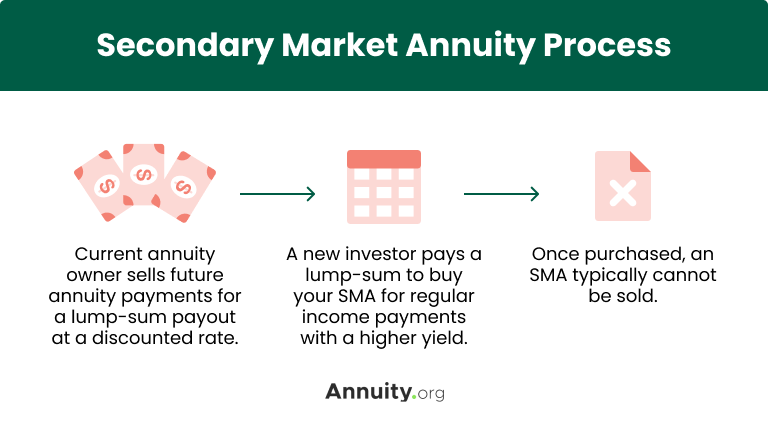

If you sell your annuity on the secondary market for a discounted lump sum, your annuity becomes a secondary market annuity (SMA). The SMA will be available for buyers to purchase, usually with a higher interest rate. A common term length for an SMA is 20 years, but it isn’t unusual to find SMAs with longer or shorter terms.

Once sold to a buyer, SMAs cannot usually be sold again. Whoever bought the SMA will receive scheduled payments while you walk away with a large lump sum.

Typically, SMAs are purchased from a third-party seller, and the courts can be involved in the selling process. For example, selling structured settlements on the secondary annuity market requires court approval.

With careful planning and risk assessment, an SMA can create a win-win situation. The annuity seller can use the large sum of cash to live comfortably in the present and the SMA buyer gains a stream of steady income to last them throughout retirement.

However, you shouldn’t sell your annuity just to have a large amount of cash on hand. You will be receiving less than the value of your total scheduled payments. So, you should have sound reasoning behind selling your annuity on the secondary market.

Common Reasons Why People Sell Their Annuities:

- Make a major life purchase (house, car or business)

- Pay off credit card debt

- Pay off medical bills

- Finance a college education or pay off student loans

- Unexpected job loss

Interested in selling some or all of your payments?

Pros and Cons of Secondary Market Annuities

Analyzing the pros and cons of SMAs from the seller and buyer’s perspective can help you understand the process.

From the seller’s perspective, the main pro of an SMA is having immediate access to a large amount of cash. The primary con is that the lump sum you receive will be less than what you were originally promised in the form of scheduled payments.

This pro will only outweigh the con if you have a dire need for the funds, such as needing to cover a health care emergency. Or, if you have a new stream of income that will keep you comfortable throughout retirement, making your annuity payments unnecessary in the long term.

Pros and Cons of SMAs from a Buyer and Seller Perspective

Seller

- Liquidity

- Freedom to cover large expenses upfront

- The lump sum will be less than the original amount of annuity payments.

- The selling process can require court approval

Buyer

- Higher yield, which is the total average annual interest rate earned with your annuity over a specified time

- Payment amount is not customizable

- SMAs are a fixed-rate investment which makes them subject to interest rate risk

- SMAs cannot usually be resold

Selling your annuity payments through an SMA provides you with a lump sum of cash that you can use for immediate needs, but often for a steep discount. It’s important to understand and weigh the tradeoffs before making that decision.

Brandon Renfro, Ph.D., CFP®, RICP®, EACo-Owner of Belonging Wealth ManagementAs a Certified Financial Planner™ professional and Retired Income Certified Professional®, Brandon Renfro is well-versed in the financial information and strategies needed to meet retirement goals. In addition to co-owning Belonging Wealth Management and assisting clients, Brandon writes regularly for financial publications.

About the Secondary Annuity Market

The secondary market started in the 1980s with financial companies acting as the “lender of last resort” for annuity owners. While the secondary market started as a riskier way to access large sums of cash, the industry has quickly developed into a profitable market for many investors.

Some examples of annuity income streams sold in the secondary market include lottery winnings, insurance money, lawsuit settlements and money from a will.

Future of the Secondary Market

A market commentary from CommonFund predicts 2023 could set a new record year for the secondary market, surpassing the $132 billion transaction volume record in 2021.

Even with inflation and rising interest rates in 2022, the secondary market recorded $108 billion in transaction volume, its second largest year ever. Even during volatile times, the secondary market can remain stable.

The long-term performance predictions for the secondary market were also positive. The same market commentary predicts the secondary market will double in size by 2026.

Secondary Market Annuities FAQs

Though secondary market annuities carry some level of risk, they are seen as a safer alternative to market-based investments. These annuities come with a payout guarantee and a fixed rate that won’t fluctuate based on the market performance.

A typical term for a secondary market annuity is 20 years.

No, you need a broker or agent to act as the middleman to buy a secondary annuity.